Wei-Loon Koe, PhD Student, Universit Teknologi MARA, 40450 Shah Alam, Selangor Darul Ehsan Malaysia, This email address is being protected from spambots. You need JavaScript enabled to view it..

Abstract

Quite ofen, people have negatve views on government-linked companies (GLCs) due to the unsatsfactory performance of some key players. In order to improve the performance of GLCs in the country, Malaysian government implemented GLC Transformaton Program (GLCT) in 2004. As the program is approaching its ending phase, some efforts are needed to assess the performance of GLCs. This study aimed to examine the influence of EO dimensions on the performance of GLCs. The sample of this study consisted of 153 subsidiaries and branches of G20. Based on the multple regression analysis performed, this study found that all the fve dimensions in EO, namely innovatveness (INNO), pro-actveness (PROA), risk-taking (RISK), compettve aggressiveness (COMP) and autonomy (AUTO) recorded signifcant positve effects on performance of GLCs. Compettve aggressiveness was identfed as the most important factor that influences the performance of GLCs. As such, all the hypotheses developed for this study were supported. The results suggested that EO is not only suitable to be applied in privately owned companies, but also in GLCs. Hence, GLCs should not be perceived as public enttes and they should be more entrepreneurial in managing their organizatons to achieve high performance. Furthermore, this study also verifed that EO is a good determinant of GLCs’ performance. At the end of this paper, recommendatons for future research have been put forth.

Keywords: entrepreneurial orientation (EO), firms, governmental-linked companies (GLCs), performance.

Introducton

Government-linked companies (GLCs) can be considered as an important driver of natonal development. In Malaysia, they account for 54% of capital market in Kuala Lumpur composite index, hire about 5% of the workforce, provide strategic utlites and services to the public, execute the country’s industrial policy, establish internatonal linkages and most importantly develop the Bumiputera community (PCG Secretariat, 2005). However, due to the poor performances of some key players such as Malaysia Airline System (MAS) and Proton Holdings, they usually give people negatve impressions (Lau and Tong, 2008). Quite ofen, general public perceives them as bureaucratc, unproftable, high in debts, low in returns and requiring multple assistance from the government.

Knowing the importance of GLCs and the unsatsfactory performance of certain major players, government has initated several strategies to improve the conditons. One of them is the unveiled GLC Transformaton Program (GLCT), a program which aims to transform GLCs into high-performing organizatons by 2015. The program was initated by Malaysian former Prime Minister Tun Abdullah Ahmad Badawi in 2004. It is worth to highlight that one of the underlying principles of GLCT is “performance focus”. Specifcally, to achieve the objectves of this program, Malaysian Directors Academy (MINDA) was established to equip the top management of GLCs with worldclass knowledge and skills for performance improvement. As the program is approaching the fnal phase of its 10-year journey, it is practcal to examine the performance of GLCs to see whether or not the program is fruitul. Moreover, improving the performance of GLCs is a critcal step in realizing the vision for compettveness and prosperity of our naton (Najid and Rahman, 2011).

Apparently, in order for GLCs to be at par with their counterparts in the private sectors, GLCs are required to change from being bureaucratc to being entrepreneurial. Entrepreneurial orientaton (EO) has been considered as a major contributor to frms’ performance. Quite a number of specialist literature such as Soininen et al. (2012a), Chen et al. (2012); Grande et al. (2011), Hameed and Ali (2011), Hafeez et al. (2011), Fairoz et al. (2010), Madsen (2007), Ripollés-Meliá et al. (2007) and Wiklund and Shepherd (2005) have found that dimensions in EO, namely innovatveness, proactveness and risk-taking had signifcant influence on performance of frms. It can be said that majority of studies on EO-performance relatonship are concentratng on the three aspects of EO mentoned above; the other two, i.e.: compettve aggressiveness and autonomy, have hardly been researched in the literature. This has yielded a lacuna in the literature.

As mentoned earlier, EO has been found as a factor affectng the performance of frms. However, studies which examine the relatonship between EO and frms’ performance are primarily using private frms or small and medium enterprises (SMEs) as the benchmark (Soininen et al., 2012a, 2012b; Hameed and Ali, 2011; Huang and Wang, 2011; Javalgi and Todd, 2011; Avlonits and Salavou, 2007; Keh et al., 2007; Tzokas et al., 2001; just to name a few). In additon, most of the studies which examined the performance of GLCs are associated with the effects of frm’s ownership (for examples, Najid and Rahman, 2011; Boubakri et al., 2009; Razak et al., 2008, 2011; Ang and Ding, 2006; Sun et al., 2002). To date, there is a paucity of studies concentratng on the influence of EO towards performance of GLCs.

To add to the above, quite a number of existng literatures on performance of GLCs are qualitatve studies; for instance, Norhayat and Sit-Nabiha (2009) have used case study in their studies. Moreover, a recent study by Omar et al. (2012) which concentrated on the effects of EO on GLCs’ performance is qualitatvely performed as well. It can be said that to date there is a lack of quanttatve empirical research focusing on GLCs performance which specifcally associated to EO.

Considering the above mentoned gaps, queston such as “are dimensions in EO influence the performance of GLCs?” stll remain unanswered. Therefore, this study is carried out with the aim to examine the influence of dimensions in EO, such as innovatveness, pro-actveness, risk-taking, compettve aggressiveness and autonomy on the performance of GLCs. The next secton of this paper provides the literature review, research framework and hypotheses. It is then followed by discussions on research methodology. Findings will be presented in the subsequent secton and the paper ends with conclusion and recommendatons.

Literature review

Government-linked Companies (GLCs) in Malaysia

The term government-linked companies (GLCs) or state-owned enterprises (SOEs) or public enterprises has been used interchangeably. Lau and Tong (2008) described GLCs as companies which are controlled by government through government-linked investment companies (GLICs), the investment arms of the government. By doing so, the government has control over the appointment of board members and senior management as well as to make major decisions such as strategic, investment and restructuring. Although GLCs are proft orientated, they are also socially and environmentally responsible (Omar et al., 2012).

Without doubt, GLCs play a signifcant role in the development of a country. For instance, according to a report released by PCG Secretariat (2005), Malaysian GLCs account for 54% of capital market in Kuala Lumpur composite index and they employed about 5% of workforce in the country. They are also the major providers of public utlites and services such as transportaton, water, power and telecommunicaton. Moreover, they are important in executng natonal industrial policy such as natonal car project, building up internatonal linkages through foreign investments and joint ventures and lastly develop the Bumiputera community.

However, the performance of GLCs is stll far from satsfactory. For long, GLCs have been labeled as underperformed, bureaucratc, monopolists, practcing favoritsm, politcally influenced or even pet government projects (The Economist, 2008). Researchers have also concluded that state-owned enterprises are less proftable and less efcient than privatzed enterprises (Boubakri et al., 2009; Ramasamy et al., 2005). In the local setng, Razak et al. (2011) have found that the fnancial performance of GLCs were not comparable to non-GLCs.

Thus, some reforms of these companies are really needed to change the people’s perceptons and also to harvest from the investment made by the people’s money. As such, a 10-year program called GLC Transformaton Program (GLCT) was launched in 2004, with the main aim to transform the GLCs into high performing organizatons by 2015. Subsequently, the Putrajaya Commitee on GLC High Performance (PCG), chaired by the Prime Minister and joined as members by heads of GLICs, was formed in 2005 to implement and oversee the initatves executed in the program. As a result, 20 large GLCs controlled by GLICs were identfed as G20 and were deemed as the focus of GLCT.

The transformaton of GLCs is important because it is closely linked to Government Economic Transformaton Program (ETP). As Najid and Rahman (2011) mentoned, improving the GLCs’ performance is important in achieving our natons’ vision for compettveness and prosperity. Currently, GLCT is at its fourth or fnal phase. The latest GLCT progress report released by PCG in 2011 unfolded that GLCs are contnuing on a growth path, with a remarkable 49% increased in growth in 2010 and have become stronger than before. Their other achievements include regionalizaton of business, improved capabilites, increased resilience, improved market percepton, developed social and economic values etc. The impressive results achieved by GLCs in recent years could be caused by the successful implementaton of GLCT. It could also caused by the entrepreneurial qualites exhibited by them. Since studies have not been extensively conducted to confrm this relatonship, this study was performed.

Entrepreneurial Orientaton (EO) and performance of frms

Entrepreneurial orientaton (EO) has been described by Lumpkin and Dess (1996: 136) as ‘processes, practces, and decision-making actvites that lead to new entry’, and ‘involves the intentons and actons of key players functoning in a dynamic generatve process aimed at new-venture creaton’. They further pointed out that the concept was comparable to entrepreneurial management (EM) by Stevenson and Jarillo (1990) and the dimensions associated to it were originated from Miller’s (1983) conceptualizaton. EO has evolved from having three dimensions, namely: (i) innovatveness; (ii) risk taking and; (iii) pro-actveness (Covin and Slevin 1989, 1991) to fve, with the other two known as compettve aggressiveness and autonomy (Lumpkin and Dess 1996).

For years, extensive studies have shown a signifcant influence of EO on performance of frms (Grande et al., 2011; Hafeez et al., 2011; Wiklund and Shepherd 2005; Covin and Slevin 1989). Specifcally, Li et al. (2009) and Ripollés-Meliá et al. (2007) have confrmed the influence of EO in listed frms and established internatonal frms respectvely. As for companies of other sizes, EO has been found as a positve and relevant contributor to increase performance among small frms (Chandrakumara et al., 2011; Keh et al., 2007). Furthermore, it has also been confrmed by many previous results as a critcal element to the success of small frms (Tzokas et al., 2001); for examples internatonal expansion (Javalgi and Todd, 2011), fnancial performance (Hameed and Ali, 2011), sales growth (Casillas and Moreno, 2010) and employment growth (Madsen, 2007) of SMEs. In the local setng, Zainol and Daud (2011) have found that EO did have a signifcant influence on performance of business frms in Malaysia.

Interestngly, some contradictng results have been obtained in studies performed by Soininen et al. (2012a), in which they found EO as an individual construct did not positvely relate to proftability. Their paper did show a positve influence of EO on growth, although such relatonship was not confrmed by Arbaugh et al. (2009). Such a mixed result has indicated the need to re-examine the EO-performance relatonship in business frms. One important insight from the above studies is that the way performance is assessed would have an impact on the EO-performance relatonship. Since frms’ performance can be determined through measuring the frms’ sales growth, market share, proftability, stakeholder satsfacton or even overall performance (Lumpkin and Dess, 1996); frms’ performance measurement should be given high atenton.

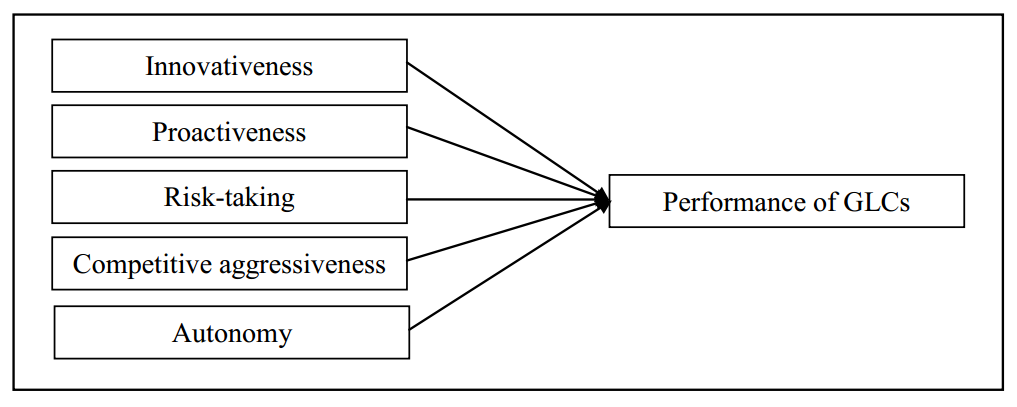

From the above discussion, the influence of EO on performance of frms in the private sector has been extensively performed. Unfortunately, the effort to extend this EO-performance relatonship on GLCs is stll low. As such, this study was conducted to shed lights on such issue. Although there were some researchers who deemed EO as a unique construct (Grande et al., 2011; Hafeez et al., 2011; Wiklund, 1999), Lumpkin and Dess (1996) have urged to view it as a multdimensional construct because the dimensions of EO may vary independently subject to the context of environment and organizaton. Following Casillas and Moreno (2010), Hughes and Morgan (2007) and Li et al. (2009), this study regarded EO as having multple dimensions, which consisted of (i) innovatveness; (ii) pro-actveness; (iii) risk taking; (iv) compettve aggressiveness and; (v) autonomy. The discussions below further explain the effects of these fve dimensions on the performance of frms. Research framework and hypotheses are presented in the following sectons as well.

Research framework and hypotheses

Innovatveness

Innovatveness is closely related to Schumpeterian “process of creatve destructon”. According to Lumpkin and Dess (1996: 142), it “reflects a frm’s tendency to engage in and support new ideas, novelty, experimentaton, and creatve processes that may result in new products, services, or technological processes.” Regardless the market instability, frms were required to sustain a contnuous state of innovatveness because innovaton played an important part in determining the performance and success of frms (Hult et al., 2004). Firms which practced innovatve behavior were found to have higher performance (Awang et al., 2009). Indeed, innovatveness has been proven positvely related to fnancial performance (Soininen, 2012b; Hameed and Ali, 2011), market share growth (Fairoz et al., 2010) and product performance (Hughes and Morgan, 2007) of frms. Similarly, Casillas and Moreno (2010) concluded higher growth rate of frms could be generated through more innovatve practces in frms. As for non-private-owned sectors, innovaton as aresult from knowledge management initatves did bring beter organizatonal performance among GLCs (Rahman and Shariff, 2009). All the studies above have unanimously agreed that innovatveness positvely affects performance and frms. Such consensus has led to the following hypothesis:

H1: There is a positve relatonship between innovatveness and performance of GLCs.

Proactveness

Pro-actveness suggests “a forward-looking perspectve that is accompanied by innovatve or new-venturing actvity” (Lumpkin and Dess, 1996: 146). Firms which possessed this quality were able to look for new business opportunites for the reason of improving their fnancial performance during recession (Soininen, 2012b). Casillas and Moreno (2010) indicated that higher proactveness promotes higher growth rate in sales, simply because frms are more aggressive in searching and capturing business opportunites. True, Fairoz et al. (2010) also found that market share growth was signifcantly affected by proactveness. This dimension which is characterized by willingness to take high-risk actons is also a vital contributor to new product performance (Avlonits and Salavou, 2007). In additon, Hughes and Morgan (2007) confrmed a signifcant correlaton between proactveness product performance and customer performance among young high-technological frms. As comparable to the previous dimension, the proactvenessperformance relatonship has reached a consensus among the previous researchers. Therefore, the hypothesis was developed as follow:

H2: There is a positve relatonship between proactveness and performance of GLCs.

Risk-taking

Assuming risk has been regarded as a quality which is very related to entrepreneurship. Risk-taking, as delineated by Lumpkin and Dess (1996: 144), includes behavior such as “incurring heavy debt or making large resource commitments, in the interest of obtaining high returns by seizing opportunites in the marketplace. Risks and returns are inseparable. For instance, Soininen et al. (2012a) concluded that the higher the risk-taking orientaton the higher the frms’ proftability. Similarly, Hameed and Ali (2011) also found a direct and distnct effect of this EO dimension on frms’ fnancial performance. Meanwhile, Fairoz et al. (2010) recorded a positve signifcant relatonship between it and market share growth. On the contrary, Casillas and Moreno (2010) did not confrm that risk-taking positvely influence growth. Hughes and Morgan (2007) also found no correlaton between risktaking and performance. During economic downturn, risk-taking was found not able to guarantee fnancial performance of frms (Soininen et al., 2012b). Interestngly, this dimension was found to have a “U”-shaped curvilinear relatonship with frms’ performance, which showed that high-risk taking frms could outperform the moderate-risk taking frms (Awang et al., 2009). Due to the inconsistencies of fndings in existng studies, it indicated that influence of risk-taking on performance of frms required a re-examinaton. As such, the hypothesis below was constructed:

H3: There is a positve relatonship between risk-taking and performance of GLCs.

Compettve aggressiveness

Compettve aggressiveness refers to “a frm’s propensity to directly and intensely challenge its compettors to achieve entry or improve positon, that is, to outperform industry rivals in the marketplace” (Lumpkin and Dess, 1996: 148). It is believed that frms which are aggressive are able to compete with their rivals in the industry and sustain their business. Researchers who have included this dimension in their EO construct have confrmed its impact on frms’ innovaton performance (Madhoushi et al., 2011). On the contrary, Casillas and Moreno (2010) found no relatonship between compettve aggressiveness and growth due to the dual-conditon, both actve and passive compettve aggressiveness. Similar result was also obtained in Hughes and Morgan (2007). The contradictng results indicated the need to re-study the effects of compettve aggressiveness on frms’ performance. Hence, the hypothesis was suggested as below:

H4: There is a positve relatonship between compettve aggressiveness and performance of GLCs.

Autonomy

Lumpkin and Dess (1996: 140) explained autonomy as “independent acton of an individual or a team in bringing forth an idea or a vision and carrying it through to completon.” The signifcant positve relatonship between autonomy and frms performance has been confrmed by Awang et al. (2009). However, such relatonship was not proven by Casillas and Moreno (2010) and Hughes and Morgan (2007). The mixed results obtained by the previous researchers showed the need to investgate the relatonship between autonomy and frms’ performance. Thus, the following hypothesis was suggested:

H5: There is a positve relatonship between autonomy and performance of GLCs.

Methodology

Populaton and sample

The sample of this study comprised of subsidiaries, including their branches of G20. The selected GLCs were represented by their respectve topmanagement such as chief executve ofcer (CEO), general manager or senior executve. It is important to note that G20 refers to GLCs which are controlled by the fve main GLICs, they are Khazanah Nasional Berhad (KNB), Permodalan Nasional Berhad (PNB), Lembaga Tabung Angkatan Tentera (LTAT), Lembaga Tabung Haji (LTH) and Kumpulan Wang Simpanan Pekerja (KWSP). Although the name G20 is given, it actually consists of 19 GLCs due to strategic exercises such as mergers, demergers and corporate restructuring. a total of 250 GLCs were selected as the sample. Of the 250 questonnaires sent, 167 were returned and 14 were unusable. Thus, the fnal sample comprised 153 GLCs. It indicated a response rate of 61.2%. The response rate was considered high and acceptable, compared to studies sampled on private frms which was about 20% to 30% (Zainol and Daud, 2011; Li et al., 2009; Hughes and Morgan, 2007) or even just around 10% (Casillas and Moreno, 2010).

Research instrument and data collecton

As this study was quanttatve in nature, questonnaire survey was regarded as appropriate. The instrument used in this study was a self-administered questonnaire. Items used by previous researchers were adapted in the questonnaire to ensure content validity of scale used. As the items originated in Western countries, slight modifcatons such as simplifcaton of complex sentences have been performed to ascertain the items ft the context of Malaysia. All items were worded in English because the respondents were top executves of GLCs, they possessed high profciency in English. In order to increase the response rate, the data collecton was conducted through a three-step process. First, the researcher e-mailed the questonnaires to respondents which held valid e-mail addresses. For the rest, traditonal mail method was used. Then, a frst-reminder was sent to the respondents afer one month and a second-reminder was sent to respondents one month afer the frst-reminder.

Variables measurements

All items for EO were adapted from Hughes and Morgan (2007), they covered the fve dimensions of EO and gauged on fve-point Likert scale (1 = “strongly disagree” to 5 = “strongly agree”). a total of 18 items were developed to capture the EO dimensions of innovatveness (INNO – three items), proactveness (PROA – three items), risk-taking (RISK – three items), compettve aggressiveness (COMP – three items) and autonomy (AUTO – six items). Meanwhile, items for frm performance were adapted from Li et al. (2009), which assessed the performance (PERF) in regards to efciency (three items), growth (three items) and proft (three items). All items used fve-point Likert scale ranged from 1 = “strongly disagree” to 5 = “strongly agree.” Efciency was determined by respondents’ satsfacton on return on investment (ROI), return on equity (ROE) and return on assets (ROA). Growth was assessed by respondents’ satsfacton on sales growth, employee growth and market share growth. Proft was measured through respondents’ satsfacton on return on sales, net proft margin and gross proft margin.

Reliability and validity

The stability or consistency of items measuring the variables, also known as reliability, can be determined through internal consistency (Sekaran and Bougie, 2009). Cronbach’s alpha (α) is considered to be the most popular indicator of internal consistency, the α-values of variables used in this study are shown in Table 1. The α-values of most variables were acceptable with α > 0.7 except for AUTO (α > 0.8), which was preferable (Pallant, 2011). In comparison, the α-values of INNO and COMP were slightly lower than Hughes and Morgan (2007); while the other two variables (PROA and RISK) had beter internal consistency reliability than the previous researchers.

| Variables | Cronbach’s Alpha (α) | |

|---|---|---|

| Current Study | Previous Study | |

| INNO | 0.71 | Hughes and Morgan (2007) = 0.81 |

| PROA | 0.76 | Hughes and Morgan (2007) = 0.75 |

| RISK | 0.79 | Hughes and Morgan (2007) = 0.77 |

| COMP | 0.74 | Hughes and Morgan (2007) = 0.75 |

| AUTO | 0.86 | Hughes and Morgan (2007) = 0.86 |

| PERF | 0.71 | N/A |

In order to ensure that the items were able to measure the desired variables, the questonnaire was validated by experts from both academics and industry sectors such as academicians and managers. Thus, face validity of the instrument was confrmed. As there were 153 sample cases in this study, conductng factor analysis to further validate the construct validity was deemed viable because it has exceeded the minimum requirement of 50 cases for factor analysis (Hair et al., 2006). Thus, exploratory factor analysis with principal components extracton and Varimax rotaton was performed for both independent and dependent variables.

For EO, the Kaiser-Meyer-Olkin value was 0.61, exceeding the minimum threshold of 0.60 (Pallant, 2011). Moreover, Barlet’s Test of Sphericity was signifcant as well (Approx. χ2 = 1474.13; df = 300 and Sig. = 0.00). Both KMO and Barlet’s statstcs verifed that factor analysis was appropriate to be conducted. The rule of Eigenvalue > 1.0 was followed and only factors with factor loading >0.5 were retained for practcal signifcance (Hair et al., 2006).

Table 2 depicts the results of factor analysis for EO. Based on the results, it was found that all items for EO have been successfully loaded into fve dimensions. The cumulatve percentage of variance explained was 63.43%, indicatng that the factors were sufcient (Hair et al., 2006).

| Items | Components | ||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| Innovatveness (INNO) | |||||

| Actvely introduce improvements and innovatons | 0.66 | ||||

| Seek out new ways of doing things | 0.60 | ||||

| Creatve in methods of operaton | 0.57 | ||||

| Proactveness (PROA) | |||||

| Take initatves in every situaton | 0.79 | ||||

| Initate actons to which other organizatons respond | 0.69 | ||||

| Excel at identfying opportunites | 0.58 | ||||

| Risk-taking (RISK) | |||||

| “Risk-taker” is considered a positve atribute | 0.73 | ||||

| Explore and experiment for opportunites | 0.54 | ||||

| Take calculated risks with new ideas | 0.52 | ||||

| Compettve Aggressiveness (COMP) | |||||

| The business is intensively compettve | 0.63 | ||||

| Take bold or aggressive approach when competng | 0.60 | ||||

| Undo and out-maneuver the competton | 0.58 | ||||

| Autonomy (AUTO) | |||||

| Freedom and independence in doing works | 0.78 | ||||

| Make and instgate changes in performing jobs | 0.77 | ||||

| Freedom to communicate without interference | 0.73 | ||||

| Authority and responsibility to act alone | 0.60 | ||||

| Act and think without interference | 0.52 | ||||

| Access to all vital informaton | 0.51 | ||||

| Eigenvalues | 3.85 | 3.09 | 2.51 | 2.12 | 1.78 |

| Cumulatve Variance Explained (%) | 17.41 | 31.78 | 43.83 | 54.30 | 63.43 |

Table 3 illustrates the factor analysis of frm performance (PERF). The KMO measure of sampling adequacy obtained was 0.77; which has passed the lowest base of 0.6 (Pallant, 2011). Meanwhile, Barlet’s Test of Sphericity was signifcant at p-value = 0.00, approx. χ2 = 351.73 and df = 25. Again, the outcomes indicated the suitability of factors analysis for PERF. All the nine items with factor loading values > 0.5 were successfully loaded into one factor. The cumulatve percentage of variance explained was 64.98%.

| Items | Component |

|---|---|

| 1 | |

| Performance (PERF) | |

| Satsfed with return on assets | 0.85 |

| Satsfed with return on equity | 0.82 |

| Satsfed with sale growth | 0.77 |

| Satsfed with employee growth | 0.76 |

| Satsfed with return on investment | 0.75 |

| Satsfed with market share growth | 0.68 |

| Satsfed with net proft margin | 0.63 |

| Satsfed with return on sales | 0.59 |

| Satsfed with gross proft margin | 0.56 |

| Eigenvalues | 4.52 |

| Cumulatve Variance Explained (%) | 64.98 |

Findings and discussions

Descriptve analysis

The informaton of the characteristcs of GLCs in this study is presented in Table 4. The results indicated that about one third of the GLCs were located in central region (N = 52, 34%), followed by southern region (N = 35, 23%), northern region (N = 29, 19%), east coast (N = 26, 17%) and only 11 GLCs (7%) were from East Malaysia. In terms of the types of industry, 63 GLCs (41%) were in servicing, 47 (31%) in manufacturing, 29 (19%) in other types of industry and 14 (9%) in agriculture. As far as their age was concerned, it was found that more than half of the GLCs were established more than 10 years ago (11 to 15 years = 41 GLCs or 27% and more than 16 years ago = 64 GLCs or 42%). It was followed by GLCs which have existed for 6 to 10 years (N = 32, 21%) and for less than 5 years (N = 16, 11%).

| Characteristcs | N = 153 | |

|---|---|---|

| F | % | |

| Locaton | ||

| Northern Region - Perlis, Kedah, Pulau Pinang and Perak | 29 | 18.95 |

| Central Region - Kuala Lumpur, Putra Jaya, Selangor and Negeri Sembilan | 52 | 33.99 |

| Southern Region - Melaka and Johor | 35 | 22.88 |

| East Coast - Pahang, Terengganu and Kelantan | 26 | 16.99 |

| East Malaysia - Sabah, Sarawak and Labuan | 11 | 7.18 |

| Type of Industry | ||

| Manufacturing | 47 | 30.72 |

| Servicing | 63 | 41.17 |

| Agriculture | 14 | 9.15 |

| Others | 29 | 18.95 |

| Years of Establishment | ||

| < 5 years | 16 | 10.45 |

| 6 – 10 years | 32 | 20.92 |

| 11 – 15 years | 41 | 26.80 |

| > 16 years | 64 | 41.83 |

Mean score and correlaton analysis

Table 5 summarizes the informaton on means and standard deviatons (S.D.) of variables and correlatons between variables. Generally, all the independent variables had mean values that ranged from 3.77 to 4.06. INNO recorded the highest mean value at 4.06 (S.D. = 0.66), while PROA noted the lowest mean at 3.77 (S.D. = 0.72). The mean value for dependent variable, PERF was 4.31 with S.D. of 0.69.

Correlaton was conducted to identfy the strength and directon of relatonship between two variables (Pallant, 2011). As this study employed interval level variables, Pearson product-moment correlaton coefcient (r) was determined (Pallant, 2011; Cooksey, 2007). As explained by Elifson et al. (1998), the r-value should range from 0 (no relatonship) to 1 (perfect relatonship). They further suggested that r-value which ranged from 0.01 to 0.30 should be considered as weak, from 0.31 to 0.70 it should be regarded as moderate and from 0.71 to 0.99 it should be interpreted as strong. However, it is important to note that all the r-values obtained were less than 0.70 (highest r = 0.64); as such, there was no problem of multcollinearity and all variables were retained (Pallant, 2011).

Results in Table 5 indicated that signifcant relatonships (p-value < 0.05) existed between pairs of independent variables, except between INNO and PROA and RISK and AUTO. In terms of relatonships between independent and dependent variables, all relatonships were found to be statstcally signifcant at p-value < 0.05. In other words, INNO (r = 0.46, p < 0.01), PROA (r = 0.18, p < 0.05), RISK (r = 0.55, p < 0.01), COMP (r = 0.64, p < 0.01) and AUTO (r = 0.33, p < 0.01) were found to be signifcantly and positvely correlated to PERF. Based on the suggeston by Elifson et al. (1998), all strengths of relatonships between PERF and EO dimensions were moderate, except for PROA which was weak.

| Mean | S.D. | INNO | PROA | RISK | COMP | AUTO | PERF | |

|---|---|---|---|---|---|---|---|---|

| INNO | 4.06 | 0.66 | 1 | |||||

| PROA | 3.77 | 0.72 | 0.23 | 1 | ||||

| RISK | 3.94 | 0.72 | 0.36* | 0.49** | 1 | |||

| COMP | 4.02 | 0.62 | 0.37* | 0.39** | 0.52** | 1 | ||

| AUTO | 3.82 | 0.77 | 0.24** | 0.46** | 0.32 | 0.31** | 1 | |

| PERF | 4.31 | 0.69 | 0.46** | 0.18* | 0.55** | 0.64** | 0.33** | 1 |

| *. Correlaton is signifcant at the 0.05 level (2-tailed). **. Correlaton is signifcant at the 0.01 level (2-tailed). |

||||||||

Multple regression analysis

There were fve hypotheses suggested in this study. In testng the hypotheses, multple regression analysis was employed. Multple regression analysis was considered as appropriate in this study because it hypothesized that more than one independent variable explained the variance in dependent variable (Sekaran and Bougie, 2009). Table 6 summarizes the results of analysis.

| Independent Variables | (β) | T-value | P-value |

|---|---|---|---|

| COMP | 0.42 | 6.68 | 0.00 |

| RISK | 0.33 | 5.63 | 0.00 |

| INNO | 0.31 | 5.96 | 0.00 |

| AUTO | 0.19 | 3.48 | 0.00 |

| PROA | 0.11 | 2.03 | 0.04 |

| R2 | 0.63 | ||

| Adjusted R2 | 0.62 | ||

| F-value | 51.28 | 0.00 |

The analysis revealed that data in this study fts the model well; it was confrmed by the F-statstcs of 51.28 and signifcant at 0.00. Thus, the relatonship between EO and PERF was statstcally signifcant. The R-square obtained was 0.63 and adjusted R-square was 0.62. This indicated that 62% of change in frm performance was affected by EO while other factors accounted for the remaining 38%. The output also showed that all the fve dimensions in EO, in which COMP (β = 0.42, p < 0.01), RISK (β = 0.33, p < 0.01), INNO (β = 0.31, p < 0.01), AUTO (β = 0.19, p < 0.01) and PROA (β = 0.11, p < 0.05) signifcantly and positvely influenced the performance of GLCs. In additon, the most important EO dimension which affected the performance of GLCs was compettve aggressiveness (COMP). As for the hypotheses testng, the results further denoted that H1 to H5 were supported.

discussion

From the statstcal analyses performed, this study found that dimensions in EO signifcantly and positvely influenced the performance of GLCs. In partcular, compettve aggressiveness (COMP) was identfed as the most important factor, which was in contrast to Casillas and Moreno (2010) Hughes and Morgan (2007). As mentoned by Lumpkin and Dess (1996), this dimension plays a vital role in ensuring the frm to outperform the other rivals in the industry. GLCs in Malaysia are not only facing competton from local privately-owned business frms, but also the internatonal giants. In additon, the pressure from government through various governmental programs, such as GLCT, has also changed the compettve landscape of GLCs in the country. The compettve conditon has defnitely caused the GLCs to aggressively and intensely seek ways to sustain in the industry.

Risk-taking (RISK) emerged as the next most important EO dimension which influenced the performance of GLCs. The fnding seemed to support Soininen et al. (2012a), Hameed and Ali (2011) and Fairoz et al. (2010), in which assuming risk is related to frms’ performance. As we know, risks and returns are closely related to each other. GLCs are backed by government; it is therefore comparatvely easy for them to obtain the necessary resources for making investment whenever they identfed new opportunites. This has defnitely resulted in bold and brave decisions in making investments by the top management of GLCs.

Innovatveness (INNO) has been evidenced by Soininen (2012b), Hameed and Ali (2011), Casillas and Moreno (2010), Fairoz et al. (2010), Awang et al. (2009), Hughes and Morgan (2007) and Hult et al. (2004) as an important determinant of frms’ performance. Similar to the previous studies, this study also found such a result and further confrmed the fndings by Rahman and Shariff (2009) in the context of GLCs. With the aim to develop an “innovaton economy”, Malaysian government has contnuously urged organizatons from both private and public sectors to be innovatve. With the establishment of governmental agencies such as Ministry of Science, Technology and Innovaton (MOSTI) and Malaysia Innovaton Agency (AIM), various fnancial and non-fnancial resources have been given to stmulate innovaton among frms. As such, there seems no reason why GLCs are not innovatve.

This study also found a signifcant relatonship between autonomy (AUTO) and performance of GLCs. Although it was in contradicton with Casillas and Moreno (2010) and Hughes and Morgan (2007), it supported Awang et al. (2009). It is believed that the minimal interference from government and clear natonal vision have helped the top management of GLCs to steer their organizatons well towards success. Lastly, similar to Soininen (2012b), Casillas and Moreno (2010), Fairoz et al. (2010), Avlonits and Salavou (2007) and Hughes and Morgan (2007); proactveness (PROA) was proven to signifcantly affect the performance of GLCs. This could be inferred by the increasing quality and ability of GLCs’ top-management in being forward-looking and seeking new opportunites.

Conclusion

This study was performed with the aim to examine the influence of fve dimensions in EO as conceptualized by Lumpkin and Dess (1996) on the performance of GLCs. It was found that about one third of GLCs in Malaysia were concentrated in the central region, majority of them were in manufacturing and servicing sectors and more than half of them were operatng for more than 10 years. Statstcal tests revealed that all the fve dimensions in EO, namely innovatveness, pro-actveness, risk-taking, compettve aggressiveness and autonomy signifcantly and positvely influenced the performance of GLCs. Compettve aggressiveness was identfed as the most important factor influencing the performance of GLCs, followed by risk-taking, innovatveness, autonomy and proactveness. Thus, all the hypotheses developed for this study were supported.

Implicatons

As mentoned by Lau and Tong (2008), people usually have negatve views on GLCs. The negatve image of GLCs is mainly caused by their inefciencies and ineffectveness in performance. This study has demonstrated that being entrepreneurial did affect the performance of GLCs. Therefore, GLCs should not perceive themselves as public enttes although they are linked to government. Contrastvely, they should regard themselves as entrepreneurs and practce entrepreneurial behavior. In partcular, they have to be aggressive in competng with compettors, take the necessary initatves and intensely seek for new opportunites are important ingredients to be highperformers. Being risk-taking, innovatve, autonomous and proactve are other entrepreneurial qualites that GLCs should possess.

Theoretcally, this study regarded EO as multdimensional instead of a unique complex construct. Thus, it shed lights on treatng EO as having fve multfaceted dimensions rather than three dimensions or simply a uniform construct because the dimensions of EO vary independently (Lumpkin and Dess, 1996). It has also showed that different dimensions possessed different strength of influence on performance of frms. As Hughes and Morgan (2007) mentoned, the relatonship between EO and frms’ performance is complex; thus, frms are required to pursue those dimensions that are deemed appropriate to improve their performance. Furthermore, it also proved that EO is not only suitable to be used in predictng performance in privatelyowned business frms, but also GLCs.

Limitatons and recommendatons

Of course, this study is not without any limitatons. There is no doubt that EO exerts direct influence on GLCs performance. However, this relatonship may be moderated or mediated by other environmental factors, for examples knowledge creaton (Li et al., 2009), learning (Wang, 2008), managerial power (Davis et al., 2010) or even family involvement (Casillas and Moreno, 2010). As such, future researchers are suggested to integrate these constructs into the EO-performance studies, specifcally to look at their moderatng or mediatng effects between EO and frms’ performance. Furthermore, this study treated performance which was measured by efciency, growth and proft as one single construct. Future studies could consider treatng them separately and look at the influence of different dimensions of EO on these three types of performance. This paper also measured performance subjectvely through the opinion of frm’s top management. Future researchers could employ an objectve method by analyzing the performance based on readily available data. Lastly, this study adopted a cross-sectonal design. As performance may be affected by the economic and other business conditons at the tme when data was collected, future research could consider a longitudinal design to see the effects of EO on performance over tme.

References

- Ang, J.S. and Ding, D.K. (2006). Government Ownership and the performance of government-linked companies: The case of Singapore. Journal of Multnatonal Financial Management, 16, 64-88.

- Arbaugh, J.B., Cox, L.W., Camp, S.M. (2009). Is entrepreneurial orientaton a global construct? a mult-country study of entrepreneurial orientaton, growth strategy, and performance. The Journal of Business Inquiry, 8(1), 12-25.

- Avlonits, G.J., Salavou, H.E. (2007). Entrepreneurial orientaton of SMEs, product innovatveness, and performance. Journal of Business Research, 60(5), 566-575.

- Awang, A., Khalid, S.A., Yusof, A.A., Kassim, K.M., Ismail, M., Zain, R.S. and Madar, A.R.S. (2009). Entrepreneurial orientaton and performance relatons of Malaysian Bumiputera SMEs: The impact of some perceived environmental factors. Internatonal Journal of Business and Management, 4(9), 84-96.

- Boubakri, N., Cosset, J.C., Guedhami, O. (2009). From state to private ownership: Issues from strategic industries. Journal of Banking and Finance, 33(2), 367-379.

- Casillas, J.C., Moreno, A.M. (2010). The relatonship between entrepreneurial orientaton and growth: The moderatng role of family involvement. Entrepreneurship & Regional Development, 22(3-4), 265-291.

- Chandrakumara, A., Zoysa, A.D., Manawaduge, A. (2011). Effects of the entrepreneurial and managerial orientatons of owner-managers on company performance: An empirical test in Sri Lanka. Internatonal Journal of Management, 28(1), 139-158.

- Chen, Y.C., Li, P.C., Evans, K.R. (2012). Effects of interacton and entrepreneurial orientaton on organizatonal performance: Insights into market driven and market driving. Industrial Marketng Management, 41, 1019–1034.

- Cooksey, R.W. (2007). Illustratng Statstcal Procedures: For Business, Behavioral and Social Science Research. Australia: The Tilde Group.

- Covin, J.G., Slevin, D.P. (1989). Strategic management of small frms in hostle and benign environments. Strategic Management Journal, 10, 75-87.

- Covin, J.G., Slevin, D.P. (1991). a conceptual model of entrepreneurship as frm behavior. Entrepreneurship Theory and Practce, Fall, 7-25.

- Davis, J.L., Bell, R.G., Payne, G.T., Kreiser, P.M. (2010). Entrepreneurial orientaton and frm performance: The moderatng role of managerial power. American Journal of Business, 25(2), 41-54.

- Elifson, K.W., Runyon, R.P., Haber, A. (1998). Fundamental of Social Statstcs. New York: McGraw Hill.

- Fairoz, F.M., Hirobumi, T., Tanaka, Y. (2010). Entrepreneurial orientaton and business performance of small and medium scale enterprises of Hambantota District Sri Lanka. Asian Social Science, 6(3), 34-46.

- Grande, J., Madsen, E.L., Borch, O.J. (2011). The relatonship between resources, entrepreneurial orientaton and performance in farm-based ventures. Entrepreneurship & Regional Development, 23(3-4), 89-111.

- Hafeez, S., Chaudhry, R.M., Siddiqui, Z.U., Rehman, K.U. (2011). The effect of market and entrepreneurial orientaton on frm performance.Informaton Management and Business Review, 3(6), 389-395.

- Hair, J.F., Black, W.C., Babin, B.J., Anderson, R.E. and Tatham, R.L. (2006). Multvariate Data Analysis, (6th Ed). Upper Saddle River, NJ: Prentce Hall.

- Hameed, I. and Ali, B. (2011). Impact of entrepreneurial orientaton, entrepreneurial management and environmental dynamism on frm’s fnancial performance. Journal of Economics and Behavioral Studies, 3(2), 101-114.

- Huang, S.K., Wang, Y.L. (2011). Entrepreneurial orientaton, learning orientaton, and innovaton in small and medium enterprises. Procedia Social and Behavioral Sciences, 24, 563–570.

- Hughes, M., Morgan, R.E. (2007). Deconstructng the relatonship between entrepreneurial orientaton and business performance at the embryonic stage of frm growth. Industrial Marketng Management, 36, 651–661.

- Hult, G.T.M., Hurleyb, R.F., Knight, G.A. (2004). Innovatveness: Its antecedents and impact on business performance. Industrial Marketng Management, 33, 429-438.

- Javalgi, R.G., Todd, P.R. (2011). Entrepreneurial orientaton, management commitment, and human capital: The internatonalizaton of SMEs in India. Journal of Business Research, 64(9), 1004-1010.

- Keh, H.T., Nguyen, T.T.M., Ng, H.P. (2007). The effects of entrepreneurial orientaton and marketng informaton on the performance of SMEs. Journal of Business Venturing, 22, 592–611.

- Lau, Y.W., Tong, C.Q. (2008). Are Malaysian Government-Linked Companies (GLCs) creatng values?Internatonal Applied Economics and Management Leters, 1(1), 9-12.

- Li, Y.H., Huang, J.W., Tsai, M.T. (2009). Entrepreneurial orientaton and frm performance: The role of knowledge creaton process. Industrial Marketng Management, 38, 440-449.

- Lumpkin, G.T., Dess, G.G. (1996). Clarifying the entrepreneurial orientaton construct and linking it to performance. Academy of Management Review, 21(1), 135-172.

- Madhoushi, M., Sadat, A., Delavari, H., Mehdivand, M., Mihandost, R. (2011). Etrepreneurial orientaton and innovaton performance: the mediatng role of knowledge management. Asian Journal of Business Management, 3(4), 310-316.

- Madsen, E.L. (2007). The signifcance of sustained entrepreneurial orientaton on performance of frms - a longitudinal analysis. Entrepreneurship & Regional Development, 19 (March), 185-204.

- Miller, D. (1983). The correlates of entrepreneurship in three types of frms. Management Science, 29, 770-791.

- Najid, N.A., Rahman, R.A. (2011). Government ownership and performance of Malaysian government-linked companies. Internatonal Research Journal of Financial and Economics, 61, 42-56.

- Norhayat, M.A., Sit-Nabiha, A.K. (2009). a case study of the performance management system in a Malaysian Government Linked Company. Journal of Accountng and Organizatonal Chang, 5(2), 243-276.

- Omar, A.R.C., Mohamad, M.R., Kader, R.A. (2012). Entrepreneurship Orientaton and Malaysian State-owned Enterprises: The Management Challenges. Proceedings in 3rd Internatonal Conference on Business and Economic Research (ICBER), March 12-13, 2012. Bandung, Indonesia.

- Pallant, J., 2011. SPSS Survival Manual: a Step by Step Guide to Data Analysis Using SPSS, (4th Ed). Australia: Allen & Unwin.

- PCG Secretariat. (2005). Catalysing GLC Transformaton to Advance Malaysia’s Development. Retrieved from: htp://www.pcg.gov.my/PDF/ PCG_Secretariat_ 29Jul05.pdf.

- Rahman, B.A., Shariff, M.N.M. (2009). Knowledge-based Malaysian GLC: Are they more innovatve and performing much beter? Malaysian Management Journal, 13(1&2), 11-19.

- Ramasamy, B., Ong, D., Yeung, C.H. (2005). Firm size, ownership and performance in the Malaysian palm oil industry. Asian Academy of Management Journal of Accountng and Finance, 1, 81-104.

- Razak, N.H.A, Ahmad, R., Joher, H.A. (2008). Ownership Structure and Corporate Performance: a Comparatve Analysis of Government Linked and Non-government Linked Companies from Bursa Malaysia. Proceedings in 21st Australasian Finance and Banking Conference, August 24, 2008.

- Razak, N.H.A, Ahmad, R., Joher, H.A. (2011). Does government linked companies (GLCs) perform beter than Non-GLCs? Evidence from Malaysian listed companies. Journal of Applied Finance & Banking, 1(1), 213-240.

- Ripollés-Meliá, M., Menguzzato-Boulard, M., Sánchez-Peinado, L. (2007). Entrepreneurial orientaton and internatonal commitment. Journal of Internatonal Entrepreneurship, 5, 65–83.

- Sekaran, U., Bougie, R. (2009). Research Methods for Business: a Skill Building Approach, (5th Ed). West Sussex, UK: John Wiley & Sons.

- Soininen, J., Martkainen, M., Puumalainen, K. and Kyläheiko, K. (2012a). Entrepreneurial orientaton: Growth and proftability of Finnish smalland medium-sized enterprises. Internatonal Journal of Producton Economics, 140(2012), 614–621.

- Soininen, J., Puumalainen, K., Sjögrén, H. and Syrjä,P. (2012b),The impact of global economic crisis on SMEs: Does entrepreneurial orientaton mater? Management Research Review, 35(10), 927-944.

- Stevenson, H.H., Jarillo, J.C. (1990). a paradigm of entrepreneurship: Entrepreneurial management. Strategic Management Journal, 11, 17-27.

- Sun, Q., Tong, W., Tong, J. (2002). How does government ownership affect frm performance? Evidence from China’s privatzaton experience. Journal of Business Finance Accountng, 29(1/2), 1-28.

- The Economist. (2005). The Malay Way of Business Change: An Atempt to Revive Malaysia’s Underperforming State-owned Firms. August 18. 2005. Retrieved 10 October 2012 from: htp://www.economist.com/ node/4307606.

- Tzokas, N., Carter, S., Kyriazopoulos, P. (2001). Marketng and entrepreneurial orientaton in small frms. Enterprise and Innovaton Management Studies, 2(1), 19-33.

- Wang, C.L. (2008). Entrepreneurial orientaton, learning orientaton, and frm performance. Entrepreneurship Theory and Practce, July, 635-657.

- Wiklund, J., Shepherd, D. (2005). Entrepreneurial orientaton and small business performance: a confguratonal approach. Journal of Business Venturing, 20, 71–91.

- Zainol, F.A., Daud, W.N.W. (2011). Indigenous (“Bumiputera”) Malay entrepreneurs in Malaysia: Government supports, entrepreneurial orientaton and frms performances. Internatonal Business and Management, 2(1), 86-99.