Dr Tomasz Kijek, University of Life Sciences, This email address is being protected from spambots. You need JavaScript enabled to view it.

Abstract

Innovaton capital regarded as an element of intellectual capital reflects the ability of an organizaton to create and commercialize the new knowledge (innovatons). The aim of this study is twofold. Firstly, an atempt is made to give a concise review of innovaton capital concept and its measures in selected intellectual capital – IC –models. Secondly, this paper sets out to extend the current models and introduce a new valuaton method of innovaton capital. Moreover, the paper provides empirical evidence about the use of the proposed method.

Keywords: innovation capital, knowledge assets, intellectual capital, measurement.

Introducton

With the increasing importance of new knowledge, innovaton capital has become the core of intellectual capital providing a powerful drive for gaining and sustaining compettve advantage (Sullivan, 1998). The results of recent studies (Wang, 2011; 2012; Chang and Hsieh, 2011) using R&D as a proxy for innovaton capital have unambiguously shown the positve relatonship between innovaton capital and the frms’ performance. Strategy literature derived from the resource-based theory (Wernerfelt 1995; Barney 1997) states that in order to fulfll a sufcient conditon for effectve managing and extractng value from innovaton capital it is necessary to recognize and measure its elements (Castro et al., 2010). A few authors (i.e. Edvinsson and Malone, 1997; Wagner and Hauss, 2000; McElroy, 2002; Chen, Zhu, and Xie, 2004) have tried to defne innovaton capital in a distnct way and propose their own categorizaton of the concept. The defnitons of innovaton capital differ from one another with relaton to the defning perspectve (i.e. technological, organizatonal or sociological) and the scope of categorizaton of innovaton capital. The differences in the defnitons of innovaton capital lead to different approaches to measuring it. But what is common to all the measurement methods is that they measure only partcular elements of innovaton capital, not the concept as a whole. Given this, the paper is intended as a review of the literature available on defning and measuring innovaton capital, as well as it introduces and validates a new valuaton model of innovaton capital.

The proposed methodology of estmatng the value of innovaton capital is based on the assumpton that it is possible to funnel a part of the value of intellectual capital to the value of innovaton - generatng knowledge assets. In the valuaton procedure innovaton capital represents a multplicatve functon/equaton of three elements, i.e. the value of intellectual capital, an extractng coefcient and an efciency coefcient. The frst coefcient allows for extractng the value of innovaton capital from the value of intellectual capital. The second coefcient represents what in Edvinsson and Malone’s (1997) terminology is called “the truth detector” of the equaton. Details on each step of the estmaton procedure are provided in the next secton of the paper.

Defnitons of innovaton capital

Innovaton capital is a term that arises from a conjuncton of two seminal economic concepts, i.e. capital and innovaton. The former is treated in neoclassical capital theory as a factor of producton that enters as an input into resources transformaton process (Birner, 2002). Most contemporary economists assume that there are two kinds of capital included in the producton functon models, i.e. physical capital and human or knowledge capital, both of which are accumulable (Arests, Palma and Sawyer, 1997). The stock of capital can render different productve services that affect its value. The later can be understood as a process (Trot, 1998; Tödtling, Lehner and Kaufmann, 2009) or an effect (Dosi, 1992; Adams, Bessant and Phelps, 2006). In the frst approach, innovaton consists of all the decisions and actvites that occur from the recogniton of a need or a problem, through research, development and commercializaton of an inventon (Rogers, 2003, p. 137). In the second approach, innovaton means the introducton of a new or signifcantly improved product (or service), process, marketng method or methods in organizatonal practces within a company, in the workplace or in foreign affairs (OECD, 2005, p. 46). In the light of the presented meanings of the concepts of innovaton and capital, innovaton capital is a bundle of the frm’s resources/assets that renders complementary services in the process of new knowledge (innovaton) creaton and commercializaton. This defniton sensu largo can be further detailed on the basis of intellectual capital – IC –theory.

There is no generally accepted defniton of innovaton capital in IC literature. One of the earliest defnitons is given by Edvinsson and Malone (1997). They describe innovaton capital as renewal capabilites of a company in the form of intellectual propertes and other intangible assets used to create and introduce new products and services to the market. There are other defnitons of innovaton capital that not only beneft from Edvinsson and Malone’s approach but also add new concepts such as learning, culture, technology and networks that are crucial in the new product/service development process. Table 1 summarizes some of the defnitons of innovaton capital introduced in IC literature.

| Defniton | Authors |

|---|---|

| The competence of organizing and implementng R&D, unremitngly bringing forth a new technology and a new product to meet customers’ demands. | Chen et al. (2004) |

| The capabilites of a company to generate value in the future. It contains the component development of processes, products and services, but also technology and management issues. | Wagner and Hauss (2000) |

| The ability of a company to develop new products, as well as any creatve ideas. | Tseng and Goo (2005) |

| A partcular archetypical social patern which aims at producton, diffusion and applicaton of new knowledge by, and for, an organizaton. | McElroy (2002) |

| Direct consequence of the company’s culture and its ability to create new knowledge from the existng base. | Joia (2004) |

| The combinaton of organizatonal knowledge necessary to develop future technological innovatons. | Castro, Verde, Saez and Lopez (2010) |

The analysis of these defnitons allows for the identfcaton of key features of innovaton capital that can be described as follows:

- Its intangibility.

- Its potental to create value in the future.

- Its reliance on technologically as well socially as embedded knowledge.

- Its excludability by property rights and trade secrets.

Moreover, these defnitons provide a useful framework for the identfcaton of innovaton capital components.

Elements of innovaton capital

In the resource-based view of a frm, innovaton capital, treated as the ability of a company to create and commercialize innovatons, can be regarded as a bundle of assets and, more generally, resources. An asset/resource is strategic if it fulflls the requirements of being valuable, seldom, immobile and not substtutable (Barney, 1997). As previously stated, innovaton capital possesses atributes that make it a “strategic asset”. For the purpose of identfying innovaton capital assets, it is important to specify the nature of these assets in relaton to the new knowledge (innovaton) generaton and commercializaton process.

According to Edvinsson and Malone (1997), innovaton capital consists of two components, i.e. intellectual property – IP and other intangible assets. Intellectual property represents legally protected and codifed knowledge that can be viewed as business assets (Sullivan, 2000). Urbanek (2008) groups IP rights into two bundles, i.e. creatve IP rights (e.g. trademarks, author rights) and innovatve IP rights (i.e. utlity models, patents). The later exist in order to protect an inventon that meets three requirements for a patent: novelty, non-obviousness and usefulness. In general, inventon is the frst occurrence of an idea for a new product or process, while innovaton is the frst commercializaton of the idea (Fagerberg, 2004, p. 4). Inventon is mainly the result of R&D actvity defned as creatve work carried out on a systematc basis in order to increase the stock of knowledge and the use of this knowledge to devise new applicatons (OECD, 2002, p. 28). It is important to note that Internatonal Accountng Standards No 38 - IAS 38 – differentate between the research and the development phases. This separaton causes that the research phase, providing (general) new scientfc or technical knowledge and understanding, is, in terms of IFRS, not regarded as an investment, which conflicts with the resource-based view of innovaton capital (Günther, 2010, p. 323). From the resources perspectve, both innovatve IP rights and R&D are in most cases the technological, codifed (registered and unregistered) knowledge assets in a portolio of innovaton capital

Another group of the elements of innovaton capital consists of intangibles that are in most cases non-technological and embodied in the organizatonal routnes and thinking of the employees. These elements can be described as follows:

- Innovaton strategy that relates to strategic choices a frm makes regarding its innovaton (Ramanujam and Mensch, 1985), i.e. the selecton of the type of innovaton that fts best the frm’s objectves and the allocaton of resources to different types of innovatons.

- Innovaton culture that is the mixture of the innovaton-related attudes, experiences, beliefs and values of the employees (Sammerl, 2006, afer: Schentler, Lindner and Gleich, 2010, p. 307). Innovaton culture has an integratng functon and stmulates innovaton actvites.

- Innovaton structure that encompasses both the innovaton process organizaton (i.e. roles, responsibilites, steps, etc) and the way the employees engaged in the innovaton are grouped (Adams et al., 2006, p. 33).

- Knowledge (technological and non-technological) possessed by the employees engaged in the innovaton process. This knowledge is tacit to varying degrees. The stock of knowledge can be increased by internal and external learning of an organizaton (Schentler et al., 2010, p. 308). Internal learning refers to the creaton of new knowledge within the enterprise, while external learning pertains to the integraton of knowledge from outside the enterprise.

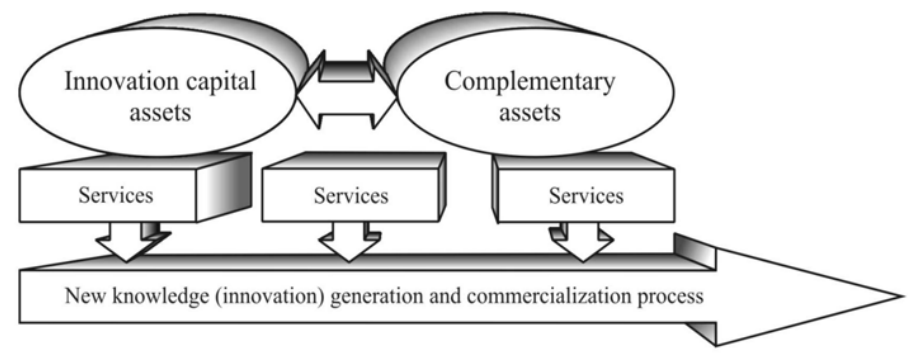

Figure 1 shows that innovaton capital assets render services in the innovaton process in combinaton with other assets of a frm such as physical assets, fnancial assets and other intangible assets. The theory and practce of the innovaton process indicate that for a successful implementaton of new inventons, the organizaton requires both the physical backup, i.e. machinery, equipment and buildings, and the fnancial one (Dodgson, Gann and Salter, 2008). In relaton to the intangibles employed in the innovaton process, Wagner and Hauss (2000) point to the dynamic interactons between the innovaton capital’s assets and other types of intangible assets. They also stress that effectve implementaton of innovatons depends on the use of all kinds of intangibles in innovaton actvity.

To sum up, innovaton capital consists of a set of resources/assets that can be regarded either as statc knowledge – potental input to the knowledge transformaton process, or dynamic knowledge – in transformaton, and fnally as the results of the knowledge transformaton process. Under this approach, the stocks of innovaton capital elements can be increased by knowledge flow from inside or/and outside of the company. For technological assets Dierickx and Cool (1989) made the distncton between the stock of technological know-how and R&D expenditure, treated as the knowledge flow, using “bathtub” metaphor. The fact that know-how depreciates over tme induces R&D spending. In case of non-technological and uncodifed knowledge assets countng of their stocks is extremely difcult. However, given the nature of these assets, Johnson (1999) argues that the use of sociological measurements may be most appropriate in this case.

Measurement of innovaton capital

In order to manage innovaton capital ratonally it must be measured and reported upon. The issue of measuring innovaton capital is important as much as it is used to develop innovaton capital assets and estmate their effect on a frm's performance (Kaplan and Norton, 1996). Therefore, there is a pressing need to measure innovaton capital from the perspectve of internal decision making. Moreover, innovaton capital measurement is necessary for communicaton with external shareholders (Mourtsen, Bukh and Marr, 2005), especially with investors seeking informaton on future performance of companies. It is important to stress that the measurement of innovaton capital is difcult, since innovaton capital assets are ofen context specifc and interconnected (Marr and Spender, 2004).

Measurement of the innovaton capital regarded as a component of intellectual capital can be performed with direct methods - DIC - and scorecard methods- SC (Roos, Pike and Fernström, 2005). Financial indicators are used as a part of the direct methods to assess the value of the elements of intellectual capital, whereas in case of the scorecard methods, non - fnancial indicators and indices are used. Table 2 presents lists of indicators of innovaton capital in both the non - fnancial approach and the fnancial one.

| Approach | Indicators |

|---|---|

| Non - fnancial | Number of new products/processes introduced in the last three years Average tme of new product/process development Number and quality of patents or patent claims Number and quality of R&D employees Cooperaton between R&D, producton and marketng departments Propensity to exchange of knowledge in social networks Management's support for innovaton culture Management ability to deal with innovaton projects Incentves for innovatve employees High management support for innovaton |

| Financial | R&D expenditures Sale of new products Income from the licensing fees |

| Source: Chen et al. (2004), Wu, Chen and Chen (2010) and Günther (2010) | |

In case of certain elements of innovaton capital, such as patents and R&D, it is possible to calculate their monetary value using the following approaches (Krostevitz and Scholich, 2010):

- Cost approach, which is based on cost assessment of an asset according to the costs needed to reproduce it or to duplicate it

- Market approach, which assumes that the value of an asset can be derived from prices obtained for similar assets in the market.

- Income approach, which estmates the value of an asset by calculatng the present value of future cash flows which are expected to be generated by the asset.

- Real opton approach, which assumes that an asset provides the company with a range of different optons. This flexibility allows the managers to avoid rigid decisions. The best known fnancial opton pricing model is the Black-Scholes model (Sudarsanam et al., 2005)

New valuaton model of innovaton capital–foundatons and calculaton procedure

The literature review on the valuaton models of intangible assets provided by Sveiby (2010) indicates that there is a lack of a model that estmates the aggregated value of innovaton capital at this point in tme. For example, Sullivan’s (2000) Intellectual Asset Valuaton – IAV model or Dow Chemical’s Citaton- Weighted Patents method (Bonts, 2001) allow for evaluaton of the innovatve IP rights but are insufcient for valuaton of innovaton capital as a whole. In turn, some of comprehensive IC measurement models such as Skandia Navigator (Edvinsson and Malone, 1997) or IC index (Roos, Roos, Dragonet and Edvinsson, 1997) tend to use and aggregate more or less consistent sets of measures of a frm’s renewal and development capacity (innovaton capital), but they are unable to give a direct fnancial value of innovaton capital, which can be easily understood and interpreted by the frm’s stakeholders. In order to reduce this gap in the literature on IC measurement, a new valuaton model of innovaton capital is introduced. Intentonally, the model is supposed to be an alternatve for measurement models of innovaton related intangibles, which take a narrow assets perspectve or use different indices aggregated in non-fnancial manner.

The proposed methodology has different areas of applicability that range from external reportng to stakeholders, through comparison among frms within the same industry to management of innovaton capital. The new valuaton model deploys widely accepted approaches to valuaton of intellectual capital, such as (Sveiby, 2010):

- Calculaton of the overall value of intangible assets, using market capitalizaton methods or return on assets methods.

- Measurement of various components of intangible assets, using scorecard methods or direct intellectual capital methods.

At the model’s foundaton is a defnitonal assumpton that intellectual capital equals the sum of human capital, structural capital, including innovaton capital, and market capital that are merely labeled differently in various IC models (Bounfour, 2002). The additve form of IC concept gives the important implicatons for the feld of IC measurement, since on the one hand it allows for a split-up of IC into a few dimensions and use of different measures covering major focus perspectves, and on the other hand it provides an opportunity for the consolidaton of all the individual indicators into a single index on a frm (Roos et al., 1997) or natonal level (Bonts, 2004). The main problem with aggregaton and disaggregaton of IC elements measured in monetary terms is the choice of measurement structure. M’Pherson and Pike (2001) argue that the additve rule for value combinaton is the excepton and suggest using conjoint measurement structures, e.g. polynomials that satsfy the combined value measurement requirement. Unfortunately, the authors do not provide convincing examples of how to measure the value effect of company’s resources interacton. In turn, Roos et al. (1997) and Schweihs and Reilly (1999) propose the employment of the additve rule (1 + 1 = 2) used as a pragmatc necessity in the aggregated value calculaton. In spite of these controversies, the additve rule for the IC value calculaton is the main point in the proposed model.

The procedure of value calculaton in this model is essentally defned by three stages:

- In the frst step of the algorithm the value of intellectual capital is calculated. The choice of valuaton method at this stage is extremely important, since it has a direct impact on the next steps and determines the fnal result of valuaton. In general, the use of a specifc measurement method depends on such factors as purpose, situaton and audience of measurement (Sveiby, 2010). Moreover, accurate, useful and defensibility of valuaton requires the selecton of a methodology applied with as much analytcal rigor as the sources of input data will allow (Sullivan, 1998). For the proposed model, the choice of IC valuaton method is limited to the market capitalizaton methods (e.g. Tobin’s Q model or the market value less the book value method) and return on assets methods (e.g. KCE model (Lev and Gu, 2011) or CIV model (Stewart, 1997)). The methods assigned to the frst group are ofen applied for an inital valuaton of intangibles in situatons of cross-companies comparisons, mergers and acquisitons or stock market valuatons. Their support for management decisions making is constrained to an organizaton’s level only (Skyrme, 2003). The methods of the second group are used in similar situatons as market capitalizaton methods but they are regarded as being more sophistcated and formally rigorous. Considering the fact that the applicaton of different methods results in values which differ, it would be recommended to utlize more than one valuaton method for a comparatve purpose.

- The second stage in innovaton capital valuaton is the extracton of the value of innovaton capital from the value of intellectual capital. This step is grounded in the additve rule for value calculaton. The proxy for the extractng coefcient is the share of new products sales in relaton to total sales. This coefcient is a direct measure of the exploitaton of innovaton capital and funnels part of the value of intellectual capital to the value of innovaton capital. It relates to innovatons that were introduced into the market and that resulted in a positve cash-flow (Kleinknecht, Montort and Brouwer, 2002). By far the share-in-sales of new products or services is one of the most commonly used measures of a frm’s innovatveness and is widely applied in empirical research (Crépon, Duguet and Mairesse 1998).

- The assessment of innovaton capital efciency. The efciency coefcient represents how effectvely an organizaton is currently using its innovaton capital and can be treated as a proxy for the quality of innovaton capital’s assets. The roots of the efciency coefcient can be found in the work of Edvinsson and Malone (1997) and according to them, it captures a frm’s velocity, positon and directons. Efciency in this model is defned as the rato of the results of innovaton capital exploitaton (e.g. number of innovatons or sales of new products or services) to innovaton capital’s assets. For the sake of calculaton correctness, the coefcient must be normalized. The method that provides relatve efciency with multple inputs and outputs is DEA (Data Envelopment Analysis). The DEA efciency of the frm is measured by estmatng the rato of virtual outputs to virtual inputs in relaton to the group of homogonous frms - Decision Making Units (Cooper, Seiford and Tone, 2007). DEA has been widely used in many applicaton areas, but recently some authors, e.g. Kijek (2010), Chen and Lu (2006), have proposed to use DEA to measure the efciency of innovaton actvity at the frm level.

Figure 2 presents the structure of the model in the form of mathematcal relatonships among its elements.

The underlying simplicity of the model allows the researchers and practtoners to adopt it in a variety of frms and sectors. The model is especially useful for knowledge based companies where the innovaton intangibles form the core assets. What is important, it provides managers and other stakeholders with the fnancial value of innovaton capital, which is especially useful for them. Moreover, the model fulfls other Lynn’s (1998) criteria for measuring intellectual capital, i.e.: it is based on informaton that is currently accessible, it uses measures that are understandable and relevant, it proposes proxies for the quality data that consttute the measured concept.

However, there are a few drawbacks of the model. The most obvious flaw is that this method is statc and relies on ex post values. Nevertheless, the model gives an opportunity to extrapolate and validate the value of innovaton capital into the future. Moreover, some controversies may arise from the concept and the calculaton of the extractng coefcient. Firstly, the coefcient concept relies on the assumpton that the value of intellectual capital can be separated into additve elements, ignoring the fact that the synergy of intangibles has a signifcant share in value creaton. Secondly, the allocaton key is arbitrary, since innovaton capital allows the company to introduce not only new products/services but also other types of innovaton. What is more, the coefcient is sensitve to the “age” of the frm, especially in case of start-up companies with an extremely high level of new product revenues. It is clear that the model has its strengths and weaknesses, and that there is a possibility for its improvement.

Methodology and results of research

In order to test the new method for the valuaton of innovaton capital, an empirical study has been conducted. In the frst stage of the study the test sample has been selected. The sample includes 9 companies from IT industry listed on NewConnect market – Polish Alternatve Stock Exchange. The companies have been ranked by investors among the 25 most innovatve frms listed on the NC market. The sample selecton was purposive, since it was important for the study to be conducted on a set of frms rich in innovaton capital. As it is known, companies in the IT sectors actvely invest in innovaton capital, which results in a high level of their innovatveness. The IT industry is classifed as a knowledge-intensive industry, where the lifespan of technology is quite short and new product introductons are frequent. As a consequence, this industry has been ofen chosen for studies on intellectual capital (Wang and Chan, 2005) and innovaton (Goswami and Mathew, 2005). Moreover, the sample has been determined by model assumptons, especially by the frms’ homogeneity requirement and by the requirement of the minimum number of DMUs in the DEA analysis (Emrouznejad and Gholam, 2009).

According to the procedure of value calculaton of innovaton capital within the model, the frst step is the valuaton of intellectual capital. This has been carried out by using the KCE model based on the classical economic theory of producton functon. Under this approach, the value of intellectual capital is estmated by subtractng the normal returns on physical and fnancial assets, from the economic performance measure – normalized earnings. The residual then becomes the contributon of intangible assets. Capitalizing the expected stream of intangibles-driven earnings over future years gives an estmate of “intangible capital.” The model formula is as follows:

VIC=(NE-α*PA-β*FA)/γ

where: VIC – value of intellectual capital (intangible capital), NE – normalized earnings, PA – physical assets, FA – fnancial assets, α – normal rate of return on physical assets, β – normal rate of return on fnancial assets, γ – discount rate of intellectual capital.

The interpretatons of the model variables, i.e. normalized earnings, physical assets and fnancial assets, have been adapted from Kasiewicz, Rogowski and Kicinska (2006). The model parameters, i.e. normal rates of return on physical and fnancial assets and a discount rate for intangibles-driven earnings, have been calibrated using the values of coefcients proposed by Lev and Gu (2011). To determine the normalized earnings I have used three-year historical data (i.e. the years 2008-2010).

Next, the extractng coefcient has been calculated as the rato of the sales of the new products or services (introduced in the years 2007-2008) to the total sales in the year 2010. The lag between the period of the introducton of new products or services and the relatve sale effects of these innovatons is consistent with a methodology of gathering data of frms’ innovaton actvity for making the NewConnect Innovatveness Ranking. The data provided by the ranking partcipants have been used in the study.

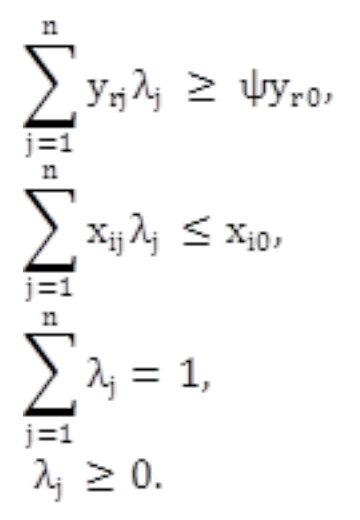

In order to calculate the efciency of the frms, the output-oriented BCC model proposed by Banker et al. (1984) has been employed. This model assumes variable returns to scale The output orientaton of the model in the study results from the assumpton that the objectve of the exploitaton of innovaton capital is to increase outputs. The model deals with one input and two outputs:

x_1j- R&D expenditure in the years 2007-2008 (as percentage of total sales).

y_1j- the number of new products or services introduced in the years 2007-2008.

y_2j- the revenues from new products or services (introduced in the years 2007-2008) in the year 2010.

The model can be expressed by the following mathematcal formulaton: ψ_0=maxψ, s.t.:

where DMUo represents one of the n DMUs under evaluaton, and xio and yro are the ith input and rth output for DMU o , respectvely. If 1/ψ*=1, then the frm under evaluaton is efcient. Otherwise, if 0<1/ψ*<1 the frm is inefcient, i.e., this frm can increase its output levels. The efciency scores in this study have been estmated using the program DEAP Version 2.1. Table 3 summarizes the results of the valuaton of innovaton capital in the selected sample of the frms.

| Firm | Value of intellectual capital [in million EUR] | Extractng coefcient | Efciency coefcient | Value of innovaton capital [in million EUR] |

|---|---|---|---|---|

| A | 3.85 | 0.65 | 1.00 | 2.50 |

| B | 3.15 | 0.04 | 1.00 | 0.13 |

| C | 0.34 | 0.47 | 0.34 | 0.05 |

| D | 0.26 | 0.44 | 0.68 | 0.08 |

| E | 1.46 | 0.85 | 0.58 | 0.72 |

| F | 0.91 | 0.38 | 0.32 | 0.11 |

| G | 0.25 | 0.52 | 0.69 | 0.09 |

| H | 0.92 | 0.08 | 0.71 | 0.05 |

| I | 0.47 | 0.84 | 1.00 | 0.39 |

| Mean | 1.29 | 0.47 | 0.70 | 0.46 |

| Std. Dev. | 1.25 | 0.27 | 0.25 | 0.75 |

Within the sample, the values of the frms’ innovaton capital differ to a great extent. For frm A with the highest value of innovaton capital, the reasons for its classifcaton are quite simple to understand and can be posited as being primarily threefold. Firstly, the frm has the highest value of intellectual capital. Secondly, its extractng coefcient is quite high. Finally, the frm is efcient in the exploitaton of innovaton capital. The problem that may arise from the calculaton procedure in this case is the size effect. A common soluton to this problem is to deflate the value of intellectual capital (Abeysekera, 2011). Nevertheless, in case of other frms the size effect is balanced by the extractng coefcient and the efciency coefcient. For instance, the second – largest frm by the value of intellectual capital (i.e. frm B) has a relatvely low value of innovaton capital in relaton to the leader because of its extremely low level of the extractng coefcient. As mentoned previously, the efciency coefcient also affects the value of innovaton capital to a signifcant extent. There are three efcient frms in the sample (i.e. frms A, B and I) and for the rest of them the values of the coefcients are less than one and indicate their level of inefciency. Moreover, on the basis of the efciency coefcient it is possible to measure the potental value of innovaton capital, assuming efciency of all frms.

The results of calculatons of the values of innovaton capital can be regarded as either strategic or operatonal objectves of innovaton capital management. For example, the frms with extremely low values of the extractng coefcient and high values of the efciency coefcient (i.e. frms B and H) should focus their atenton on how to reformulate the innovaton strategy to achieve the potental value of innovaton capital. In turn, the frms that are inefcient in exploitng their innovaton potental (i.e. frms C and F) ought to analyze the process of innovatons implementaton and identfy the areas, i.e. the elements of innovaton capital, for improvement.

Summarizing the results of the research, it should be noted that they are limited to the sample frms. The study allows for illustratng how the model helps to reveal the value of intangible assets rendering services in the innovaton process. Moreover, the research fndings supply the opportunity to identfy “best practces” in relaton to the exploitaton of innovaton capital within the sample. Although the model provides a rough value of innovaton capital, the results of its applicaton may be a startng point for a further, more detailed, valuaton of the elements of innovaton capital.

Conclusions

This paper produces a few important contributons to the theory of innovatonrelated intangibles. Theoretcal implicatons of this work concern two subject areas: the literature on defning and categorizaton of innovaton capital and the literature on measuring innovaton capital.

In the frst case, the paper provides the working defniton of innovaton capital, derived from the theory of capital and the theory of innovaton, and identfes its key features. In additon, this work offers a new classifcaton of the innovaton capital’s elements. The proposed classifcaton goes beyond the narrow focus approaches, typical for most of IC models, since it includes a broad set of knowledge assets ranging from the technological assets to the tacit knowledge embedded in employees.

In the second case, this paper introduces a new valuaton model of innovaton capital with its own calculaton procedure. The new valuaton model is based on the assumpton that it is possible to funnel a part of the value of intellectual capital to the value of innovaton capital. The model consists of a three - stage algorithm. The value of innovaton capital is estmated as a result of multplying three elements, i.e. the value of intellectual capital, the extractng coefcient and the efciency coefcient. From the methodological point of view, the method is an incremental innovaton in the literature on intangibles measurement, but underlying simplicity of the model makes it useful for managers and other stakeholders and as Skyrme (2003) comments on the stage of IC measurement development: “Here, simplicity can be a virtue” (p. 239).

Considering the managerial implicatons, it is worth emphasizing that the model use may facilitate the process of innovaton capital management by increasing manager’s understanding of the contributon of innovaton capital into a company’s performance. It seems to be extremely important for managers that innovaton capital is measured in monetary terms in the model. This helps managers to focus their atenton on the increase of the value of innovaton–related intangibles. What is important, the results of the value of innovaton capital estmaton within the sample are useful in the processes of searching for best practces and identfcaton of the areas and means of performance improvement. Moreover, the model provides more relevant informaton to investors and analysts on the company’s innovaton capacity than traditonal, single measures of innovaton capital such as R&D or patents. Thus, the model may be deployed to a process of fundamental analysis to support the stock price forecastng.

The results of the model applicaton in the sample of the IT frms are very interestng and can be regarded as an illustratve example of the model use. Moreover, the results of the study provide an opportunity to comparatve analyses. Because this study has been conducted on the sample of the frms listed on the Polish alternatve trading system, the results may be used as a benchmark for the comparison of the value of innovaton capital of IT frms listed on other European or American alternatve trading systems. Although the results seem to be informatve, they have some limitatons. Firstly, as previously noted, the model has been trialed with a limited number of companies form the IT industry. Secondly, the KCE model of calculatng the value of intellectual capital has several drawbacks (Ujwary-Gil, 2009). Thirdly, the number of inputs (i.e. the elements of innovaton capital) in DEA model used to estmate the efciency coefcient is relatvely small. Instead, there are several other elements of innovaton capital beyond the scope of this study that may be included in DEA analysis.

Due to the above limitatons, further research on the model applicaton is needed. The interestng new pathways for the future are: extending the scope of research to work with a statstcally signifcant sample, using other models of the valuaton of intellectual capital in the frst step of the valuaton algorithm and broadening a set of inputs in the DEA method so as to include more elements of innovaton capital in the process of estmatng the efciency coefcient. I believe that in this way the model may provide more accurate values of innovaton capital.

References

- Abeysekera, I. (2011). The relaton of intellectual capital disclosure strategies and market value in two politcal setngs. Journal of Intellectual Capital, 12 (2), 319-338.

- Adams, R., Bessant, J. and Phelps, R. (2006). Innovaton management measurement: A review. Internatonal Journal of Management Reviews, 8 (1), 21-47.

- Arests, P., Palma, G. and Sawyer, G. (1997). Capital Controversy, Post-Keynesian Economics and the History of Economic Thought: Essays in Honour of Geoff Harcourt. London: Routledge.

- Banker, R.D., Charnes, A. and Cooper, W.W. (1984). Models for the estmaton of technical and scale inefciencies in Data Envelopment Analysis. Management Science, 30, 1078-1092.

- Barney, J. (1997). Gaining and Sustaining Compettve Advantage. New York: Addison – Wesley Publishing Company.

- Birner, J. (2002). The Cambridge Controversies in Capital Theory: A Study in the Logic of Theory Development. London: Routledge.

- Bonts, N. (2001). Assessing knowledge assets: a review of the models used to measure intellectual capital. Internatonal Journal of Management Reviews, 3 (1), 41–60.

- Bonts, N. (2004). Natonal Intellectual Capital Index: A United Natons initatve for the Arab region. Journal of Intellectual Capital, 5 (1), 13-39.

- Bounfour, A. (2002). The Management of Intangibles: The Organisaton's Most Valuable Assets. London: Routledge.

- Castro, G., Verde, M., Saez, P. and Lopez, J. (2010). Technological Innovaton. An Intellectual Capital Based View. Basingstoke: Palgrave Macmillan.

- Chen, J., Zhu, Z. and Xie, H. (2004). Measuring intellectual capital: a new model and empirical study. Journal of Intellectual Capital, 5 (1), 195-212.

- Chen, T. and Lu, L. (2006). Innovaton and the operatonal performance of IC design industry in Taiwan: a data envelopment analysis model. Paper presented at 15th Internatonal Conference on Management of Technology, Beijing, China.

- Cooper, W., Seiford, L. and Tone, K. (2007). Data Envelopment Analysis. New York: Springer.

- Crépon, B. Duguet, E. and Mairesse, J. (1998). Research, Innovaton, and Productvity: an Econometric Analysis at the Firm Level. Economics of Innovaton and New Technology, 7, 115-158.

- Dodgson, M., Gann, D. and Salter, A. (2008). The Management of Technological Innovaton: Strategy and Practce, Oxford: Oxford University Press.

- Edvinsson, L., and Malone, M.S. (1997). Intellectual Capital: The Proven Way to Establish Your Company's Real Value by Measuring Its Hidden Brainpower. London: Judy Piatkus.

- Fagerberg, J. (2004). Innovaton: A Guide to the Literature. In: J. Fagerberg, D. Mowery and R. Nelson (Ed.), The Oxford Handbook of Innovaton (pp. 1-25). Oxford: Oxford University Press.

- Günther, T. (2010). Accountng for Innovaton: Lessons Learnt from Mandatory and Voluntary Disclosure. In: A. Gerybadze, U. Hommel, H.W. Reiners, and D. Thomaschewski (Ed.), Innovaton and Internatonal Corporate Growth (pp. 319-332). Berlin: Springer.

- Goswami, S. and Mathew, M., (2005). Defniton Of Innovaton Revisited: An Empirical Study On Indian Informaton Technology Industry. Internatonal Journal of Innovaton Management, 9 (3), 371-383.

- Kaplan, R.S., and Norton, D.P. (1996). The Balanced Scorecard: Translatng Strategy into Acton. Boston: Harvard Business School Press.

- Kasiewicz, S., Rogowski, W. and Kicińska, M. (2006). Kapitał intelektualny. Spojrzenie z perspektywy interesariuszy. Warszawa: Ofcyna Ekonomiczna.

- Kijek, T. (2011). Evaluaton of efciency of enterprises’ innovaton actvity. Economics and Organizaton of Enterprise, 1, 24-32.

- Kleinknecht, A., Montort, K. and Brouwer, E. (2002). The Non-Trivial Choice between Innovaton Indicators. Economics of Innovaton and New Technology, Vol. 11 No. 2, pp. 109-121.

- Krostewitz, A. and Scholich, M. (2010). Modern Valuaton Approaches for Corporate Innovaton Actvites. In: A. Gerybadze, U. Hommel, H.W. Reiners, and D. Thomaschewski (Ed.), Innovaton and Internatonal Corporate Growth (pp. 263-280). Berlin: Springer.

- Lev, B. and Gu, F. (2011). Intangible Assets: Measurement, Drivers, and Usefulness. In: G. Schiuma (Ed.), Managing Knowledge Assets and Business Value Creaton in Organizatons: Measures and Dynamics (pp. 110-124). Hershey: IGI Global.

- Lynn, E. (1998). Performance evaluaton in the new economy: bringing the measurement and evaluaton of intellectual capital into the management planning and control system. Internatonal Journal of Technology Management, 16 (1-3), 162-176.

- Marr, B. and Spender, J. (2004). Measuring knowledge assets – implicatons of the knowledge economy for performance measurement. Measuring Business Excellence, 8 (1), 18 – 27.

- McElroy, M. (2002). Social innovaton capital. Journal of Intellectual Capital, 3 (1), 30-39.

- Mouritsen, J., Bukh, P.N. and Marr, B. (2005). A reportng perspectve on intellectual capital. In: B. Marr (Ed.), Perspectves on Intellectual Capital (pp. 69-81). Oxford: Buterworth-Heinemann.

- M’Pherson, P. K. and Pike, S. (2001). Accountng, empirical measurement and Intellectual Capital. Journal of Intellectual Capital, 2 (3), 246–260.

- OECD (2005). Oslo Manual: Guidelines for Collectng and Interpretng Innovaton Data. Luxembourg: OECD Publishing. OECD (2002). Frascat Manual 2002: Proposed Standard Practce for Surveys on Research and Experimental Development. Luxemburg: OECD Publishing.

- Ramanujam, V. and Mensch, G.O. (1985). Improving the strategy–innovaton link. Journal of Product Innovaton Management, 2, 213–223. Rogers, E.M. (2003). Diffusion of Innovatons. New York: Free Press.

- Roos, J., Roos, G., Dragonet, N.C. and Edvinsson, L. (1997). Intellectual Capital: Navigatng in the New Business Landscape. London: Macmillan.

- Roos, G., Pike, S. and Fernström, L. (2005). Managing Intellectual Capital in Practce. Oxford: Buterworth-Heinemann.

- Sammerl, N. (2006). Innovatonsfähigkeit und nachhaltger Wetbewerbsvorteil: Messung, Determinanten, Wirkungen. Wiesbaden: DUV.

- Schentler, P., Lindner, F. and Gleich, R. (2010). Innovaton Performance Measurement. In: A. Gerybadze, U. Hommel, H.W. Reiners, and D. Thomaschewski (Ed.), Innovaton and Internatonal Corporate Growth (pp. 299-317). Berlin: Springer.

- Skyrme D. (2003). Measuring knowledge and intellectual capital. London: Optma Publishing.

- Stewart, T.A. (1997). Intellectual Capital: The New Wealth of Organizatons. New York: Doubleday.

- Sudarsanam, S., Sorwar, G. and Marr, B. (2005). A Finance Perspectve on Intellectual Capital. In: B. Marr (Ed.), Perspectves on Intellectual Capital, ButerworthHeinemann (pp. 56-68). Oxford: Buterworth-Heinemann.

- Sullivan, P.H. (1998). Proftng from Intellectual Capital. Extractng Value from Innovaton. New York: John Wiley&Sons.

- Sullivan, P.H. (2000). Value-Driven Intellectual Capital: How to Convert Intangible Corporate Assets Into Market Value. New York: John Wiley&Sons.

- Sveiby, K. (2010). Methods for Measuring Intangible Assets. Retrieved from htp://www. sveiby.com/artcles/IntangibleMethods.htm

- Tödtling, F., Lehner, P. and Kaufmann, A. (2009). Do Different Types of Innovaton Rely on Specifc Kinds of Knowledge Interactons?. Technovaton, 29, 59–71.

- Trot, P. (1998). Innovaton Management and New Product Development. London: Financial Times Management.

- Tsen, C. and Goo, Y. (2005). Intellectual capital and corporate value in an emerging economy: empirical study of Taiwanese manufacturers. R&D Management, 35 (2), 181-207.

- Ujwary-Gil, A. (2009). Kapitał intelektualny a wartość rynkowa przedsiębiorstwa. Warszawa: C.H. Beck.

- Urbanek, G. (2008). Wycena aktywów niematerialnych przedsiębiorstwa. Warszawa: PWE.

- Wagner, K. and Hauss, I. (2000). Evaluaton and Measurement of R&D Knowledge in Engineering Sector. In: M. Khosrowpour (Ed.) Proceedings of the 2000 informaton resources management associaton internatonal conference on Challenges of informaton technology management in the 21st century (pp. 709-712). Anchorage: Idea Group Publishing.

- Wang, M. (2012). Could Innovaton Capital impact On Firm Performance? Study by Panel Data Two Stage Regression with Board Compositon. Applied Mechanics and Materials, (145), 430-435.

- Wernerfelt, B. (1995). The resource-based view of the frm: Ten years afer. Strategic Management Journal, 16 (3), 171-174.

- Wu, H., Chen, J. and Chen, I. (2010). Innovaton capital indicator assessment of Taiwanese Universites: A hybrid fuzzy model applicaton. Expert Systems with Applicatons, 37, 1635-1642.