Dra. Rocío Durán-Vázquez, Department of Finance and Accountng, Universidad de las Américas Puebla, Exhacienda Santa Catarina Mártr s/n, This email address is being protected from spambots. You need JavaScript enabled to view it..

Dr. Arturo Lorenzo-Valdés, Department of Finance and Accountng, Universidad de las Américas Puebla, Exhacienda Santa Catarina Mártr s/n, This email address is being protected from spambots. You need JavaScript enabled to view it..

Dr. G.Einar Moreno-Quezada, Department of Finance and Accountng, Universidad de las Américas Puebla, Exhacienda Santa Catarina Mártr s/n, This email address is being protected from spambots. You need JavaScript enabled to view it..

Abstract

This study analyzes the behavior of the companies in the index of México’s Precios y Cotzaciones (IPC), with respect to measures of fnancial performance and its relatonship with the two main approaches of innovaton, according to the Bogota and Oslo manuals; assessing their impact on the stock price. The data is used on a quarterly basis from January 2000 to December 2011. It also makes reference to the impact of having the distncton “Socially Responsible Company” (Corporate Social Responsibility), in the Mexican stock market price reacton. Our main interest is to be pioneers in the search for relatonships between topics that are currently treated as “alien” (CSR and Innovaton) in formal academic publicatons, but we intuitvely know that they are related inside organizatons.

Keywords: value of relevance, innovation and financial, distinctive of corporate social responsibility.

Introducton

The current business environment has highlighted the importance of incorporatng innovaton, both as a guide for surviving in the day to day operaton as part of the strategy of long-term positoning. The literature contains evidence that supportng innovaton brings about the economic growth of businesses and this is shown in a beter fnancial performance.

Internatonally criteria on innovaton are included in Oslo Manual, where the main points identfy what innovaton is (in the context of business operatons) and measure land concepts and elements to design survey instruments. In Latn America, we have the manual specifcally referring to Bogota and Mexico, the Natonal Council for Science and Technology (CONACYT), which has conducted surveys on innovaton performance, under the approach of these two manuals (Oslo and Bogota). Partcularly in the 2001 survey it was applied in manufacturing and service companies with over 50 employees, by the Natonal Insttute of Statstcs, Geography and Informatcs (INEGI). In this study they highlighted the approach to public companies.

There are different approaches to innovaton studies of public companies, regarding the measurement of the number of patents or new brands (about new product or services) or referring to research and development expenses (R&D) or to cost reductons (by implementng new processes of operatve’ efciency). In this study we began the analysis with exploratory econometrical tests of the impact on fnancial statements informaton, as a proxy, we identfy evidence of the impact of innovaton in two ways: frst, cost reductons (measured by the decrease on operatve expenses on the Income Statement), second, new long term investment in terms of new plant or equipment acquisiton that support new product or service´ characteristcs to offer (measured by the increase on fxed assets on the Balance Sheet). This proxy is a general consideraton of the two main characteristcs of innovaton that we defne on Stakeholders of affectve management secton.

This approach offers the opportunity to document the measurement of innovaton, from the published data of the companies listed on the Mexican Stock Exchange (BMV), reflectng the aggressive strategy (identfed as increased investment in the long term) and defensive strategy (identfed as the efciency of the current operaton), and we analyze whether the market perceives and rewards it or not, (in response to the stock price of public companies). Specifcally, the study covers the period 2000 to 2011 with data members IPyC Mexican companies (Index of Prices and Quotatons) of the BMV.

Besides, we added a third variable to the analysis: the distnctve of Corporate Social Responsibility (CSR), as an additonal recogniton of the practces of the public companies, in order to identfy if there is an impact of this variable on the share return in the stock market. We decided to add this variable as complement to the exploratory analysis of the study, because we suspect that the companies with the CSR distnctve follow some criteria of innovaton implementaton and we test the reference of the correlaton between the variables under panel data models (in Discussion appears the econometrical results). This idea is supported under the premise that the public companies of Mexico are the biggest ones and usually the leaders of their economic sector actvity.

The CSR award (identfed in Spanish as ESR for “Empresa Socialmente Responsable”) has taken 11 years to bestow itself in Mexico. It is awarded annually by the CEMEFI (Mexican Center for Philanthropy, Civil Associaton, a young group with more than 20 years of existence), in conjuncton with AliaRSE (Alliance for Corporate Social Responsibility in Mexico). This badge is awarded in recogniton of conscious commitment and consistent enforcement of business ratonale, covering both internal and external goals, expectatons considering economic, social and environmental impacts of all partcipants (which are related to the company), in pursuit constructon of the common good.

Abreu (2009) emphasized that "[...] in Mexico, Corporate Social Responsibility and philanthropic initatve began, but in the 90's it changed into the reflecton that philanthropy is not enough to promote social progress" . And Market (2007) defnes Corporate Social Responsibility as “… a working model and organizaton that brings back to society what the company makes, it is a way of doing business in a sustainable manner."

Theoretcally it is considered that this flag provides real and tangible benefts for the company, which can be measured in different ways, based on quanttatve and qualitatve evidence which is found in studies such as Accenture (2010). This study highlights the quanttatve impact, partcularly public companies in the stock price three months afer obtaining the label.

The highlights that CEMEFI consider about clients is that when they are choosing between two brands of the same quality and price, the issue of social responsibility is the most affected in the purchase decision, according to their studies it represents 41% and is followed by design and innovaton (32%) and brand loyalty (26%). What's more, 70% of consumers say they are willing to pay more for a brand that supports CSR causes.

The aim of this study is to conduct an exploratory study of fnancial accountng variables (of the quarterly fnancial statements) of the companies comprising the Index of Prices and Quotatons (IPyC) of the Mexican Stock Exchange (BMV), seeking to reflect the impact of business innovaton efforts (in the light of internatonal manuals Oslo and Bogotá). Additonally we evaluate the impact of having the distnctve of Corporate Social Responsibility (CSR) given by Mexican Center for Philanthropy, AC (CEMEFI), in the stock price. And the relevance of it is to identfy the interrelaton between the considered variables, measured by the signifcance on the returns of share price in the stock market. This impact is tested (on the dependent variable of the models) three months later (because we are measuring the change on fnancial statements), in literature the impact of innovaton or the CSR are usually considered on the strategy and positon of the company on the market in the long term, but that is another approach. There is a lack of reference in this feld, so these results present inital evidence of this kind of quanttatve analysis, that’s why we performed econometric tests; we are not following a qualitatve discussion of it.

Innovaton and fnancial performance

Strategic references of innovaton

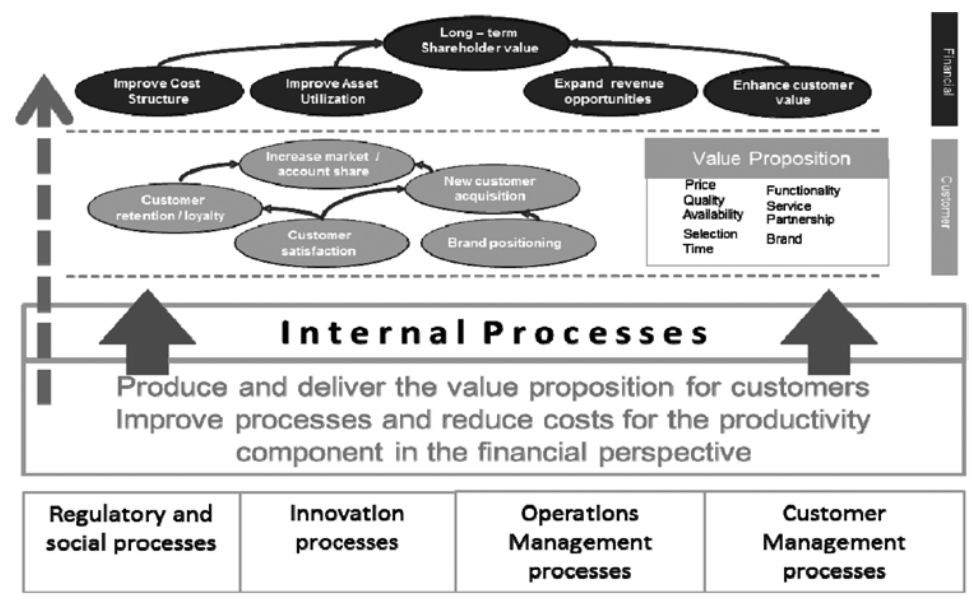

In Mexico, like in other countries, doing business has partcular characteristcs. We must remember the line: “You can´t manage what you can´t measure”. This message is the base of the theory of performance measurement. As a mater of fact, specialists like David Norton and Robert Kaplan, creators of the “Strategic Maps Model”, like to use a special piece of one of the most successful heuristcs in the last years to align efforts in the organizatons: The Balanced Scorecard (BSC) from Kaplan and Norton, (1996).

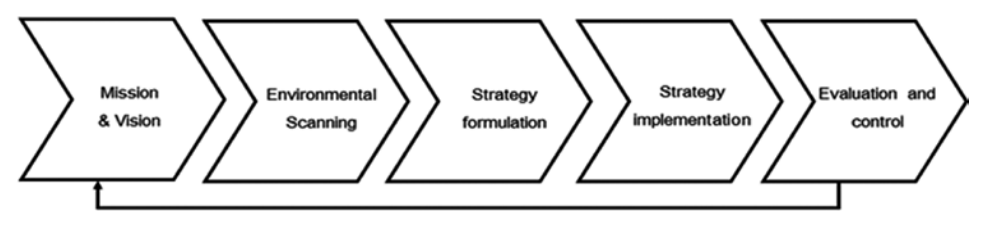

But, why is this heuristc so successful? The answer begins when we review the original design of the strategic maps. First, we must remember the original strategic planning process:

The only way to know if a strategy is the correct one is by executng it. Therefore, we must have a tool which allows us design strategies and evaluate them in a way that we will easily and quickly notce its efciency. Only in this way, and hence, it will be used as support in decision-making processes to adjust it or modify it partally or totally, as we present in Figure 2.

Strategic maps are the ones which allow us to design different possible strategies. By using causal relatonships among objectves within the Finance, Clients, Processes and Learning perspectves, BSC assigns indicators to each driver within the map to determine if it is, “per se”, moving forward in the frst place, and, in the second place, if the desired consequence is being generated.

It is important to point out that within the process perspectve; innovaton is a very well specifed topic. Although we are aware of the existence of many different schools that specialize in this topic and its partcularites, our interest is to prove how, even in a model like this, innovaton occurs in the foreground. Topics such as research and development opportunites, launching new products, materializaton of new projects, number of developed patents and certfcatons achieved are initatves that may be included in this topic.

Afer designing the indicators, goals are established and last, projects are assigned. In this way, we are able to read in just one document how all the organizaton’s actvites are aligned towards fnancial results in terms of sales and profts.

One of the biggest challenges of BSC is fnding the drivers (BSC’s methodology) which are the real causes of the desired consequences in the fnancial perspectve. What process will be a key to generate more sales or profts as a consequence? Which type of training is required to ensure that process? How do we know if the value innovaton in which the organizaton is currently working on will be perceived by the client and will ultmately lead to proft increase?

To address these questons, BSC methodology incorporates the design of tendency and result indicators which are meant to measure the drivers’ progress and to verify the causal relatonships between them, as in Iselin and Sands (2008). From training days to hours per client, product mix, even market share, all are indicators built according to each driver.

The indicators must have, among others, four main characteristcs so that they truly support us in the strategic tracing, as in Cardinaels and Van Veen-Dirks (2010):

- Measurable, in a way that it is easy to tract them.

- Actonable, which is, affected by critcal business actons.

- Practcal, that is, they make sense just as they are defned to be used and,

- Relevant, which means, they reflect drivers’ improvements or worsening

This empiric way of checking the progress in the strategy lies largely in one of the challenges of using follow-ups for the BSC. The BSC methodology even proposes (and given that in many organizatons it is common to fnd huge lists of Key Performance Indicators) performing a prioritzaton matrix to keep initally only the KPIs which satsfy the four characteristcs previously discussed, as in Yu, Perera and Crowe (2008).

This is where it is very useful to have mathematcal models which help us corroborate our qualms about the causal relatonships required at the moment of executng a strategy.

Finally, in our country the organizatons have developed and implanted different actons in an effort to increase the fnancial outcomes. In that way, as a part of their strategy, they bet on the fact that the actons are correct. Is this true?

Internatonal Manuals of reference

The Oslo Manual, which is aligned with the OECD (Organizaton for Economic Cooperaton and Development), defnes four types of innovaton: product, process, organizatonal and marketng. This classifcaton is consistent with the list submited by Schumpeter (1934), which was the start of this research, focusing on both the analysis of this feature, and the design of surveys to measure precisely to innovaton.

And what do we mean by innovaton? According to the above classifcaton, innovaton implies the introducton of a new or signifcantly improved product (good or service), improvement of a process, a new marketng method or a new organizatonal method in the frm's internal practces, the organizaton of the workplace or external relatons.

In this paper we consider only the frst two: product (considering the long-term investment in order to be cutng edge) and process (considering the operatng efciency of the company).

The choice of approach to the study of innovaton can be based on the "subject" or "object". The subject is about the innovatve actvites of the company as a whole and the object-based approach involves analysis from specifc innovatons, for this work we chose the approach of "subject".

Why do companies innovate? To improve performance, either by increasing demand or reducing costs. In terms of corporate strategy innovaton in its operatonal decisions: both in terms of product (providing that good or service and novelty differentated from the competton) and in regard to processes (searching efciency operaton).

The frst aspect requires a long-term investment in either tangible or intangible resources that produce benefts in the short and long term, in terms of producton and sale of the product (this is reflected in the amount of investment allocated for it). Companies will therefore be reinvestng in the business, looking to have noveltes in the "product (or service)" in the market, translated into strategy involving a differentatng leader.

The second focuses on reducing costs and operatng expenses of the company, in terms of a mechanism applying contnuous improvement or administratve control (this is reflected in the reducton of operatng expenses of the company). Companies will thus improve their business internally in every process; strategy can be translated into a leader in low compettve price or a follower (by reducing internal costs and expenses).

Corporate social responsibility and fnancial performance

One issue that has recently become more important is the practce of corporate social responsibility; currently companies not only aim at generatng profts but also at ensuring that their operatons are sustainable economically, socially and environmentally.

Taking into account the extent to which the behavior and expectatons of the society change, organizatons are stll in the middle of the last century when there are early signs of what is now known as corporate social responsibility, however, it was only in the 70's that term began to be used, since in this period investors became aware of the power of money, using it as an instrument of pressure against companies supportng any war or politcal decision detrimental to a vulnerable group of society or different values and moral principles, achieving through this strategy is concerned and occupaton of the damage to the environment of society.

This causes the need for a regulaton to this practce, originatng in the year 1977 to CEPAA (Council Economic Priorites Accreditaton Agency) issuing a voluntary standard: "Social Accountability", in ensuring the ethical producton of goods and services with core human rights codes and working conditons, so as to achieve this standard requires companies before entering the ISO 9000 quality standard that promotes contnuous improvement in the standard necessary aspects Social Accountability.

Since 2000 investors realize the proven practces of Corporate Social Responsibility, give evidence of quality management and corporate governance.

Taking into account the above we can contextualize CSR as "meet the main goal of the company (as Milton Friedman are economic performance), while considering the social, environmental, and economic impacts of their partcipants through ethical practce, and promotng the common good.

One should also menton the creaton of ISO 26000 in 2010, by the Internatonal Organizaton for Standardizaton, prepared by ISO / TMB Working Group on Social Responsibility, which is intended to provide guidance to all types of organizatons did sustainable development that go beyond legal compliance, drawing on the practce of social responsibility with support systems, policies, organizatonal structures and existng networks.

To implement this policy it is essental to know that the partcipants related to the organizaton and society are stakeholders, promote effectve involvement in them, based on good faith and true dialogue, a different reason for the independent judgment of each party. Similarly, menton is made of seven principles which will enable the company to meet sustainable development, which is the primary goal of a socially responsible organizaton. These are:

- Accountability: what the organizaton must answer about their decisions and actvites.

- Transparency: an organizaton should disclose clear, accurate and tmely informaton to enable stakeholders to evaluate the impact that the decisions and actvites of this produce on their interests.

- Ethical behavior: involving values and commitment for people, animals and environment.

- Respect the interests of stakeholders: consideraton and response to the interests of stakeholders.

- Respect for the law: no individual or organizaton is above the law.

- Respect for internatonal norms of behavior. An organizaton should strive to meet minimum internatonal standards of behavior.

- Respect for human rights: by recognizing its importance and universality.

Once the organizaton is aware of the importance of social responsibility for itself and its environment, you must frst go through an internal process of understanding, beginning with:

- Diligence. Comprehensive and proactve process carried out to identfy the negatve impacts of decisions and actvites within an organizaton, in order to prevent and mitgate such impacts.

- Relevance. Is about to review all the key actvites in order to identfy which issues are relevant.

- Importance. Is the decision of which issues are the most signifcant, and most important to the organizaton, taking into account the extent of impact on stakeholders and sustainable development.

Having completed the above steps, it is appropriate to draw on the success of the organizaton that has influence on the ownership and governance, the economic, the legal authority / policy and public opinion, grounded on factors such as physical proximity, scope, the duraton and strength of the relatonship by promotng awareness about social responsibility and socially responsible behavior.

Because of this, several countries have created organizatons to encourage their exercise, speaking in the natonal context,CEMEFI (Mexican Center for Philanthropy AC) was created in 1988. It is a private, nonproft, founded as a civil partnership, and it is the main body responsible for corporate social responsibility in Mexico, using tools such as CSR and Recogniton Best Practces in CSR (corporate social responsibility), some of its objectves are to promote and coordinate the philanthropic partcipaton, engaged and socially responsible citzens, social organizatons and enterprises to achieve a more equitable, fair and prosperous society, and have effectve tools and mechanisms of linkage, and join alliances between philanthropic sector actors and other sectors in order to achieve a more equitable society.

Currently there are some concerns on the issue of social responsibility, as whether the practce of it in a company influences its fnancial performance, some people mentoned that their exercise in an organizaton brings benefts such as atractng and retaining talented workforce, improved compettveness and market positoning, the interest of investors and thus access to capital.

That is why in this paper we apply an econometric model to analyze the relatonship between socially responsible companies in Mexico and its fnancial performance.

Since 1971 there have been multple studies aimed at fnding the relatonship between corporate social responsibility and fnancial performance, obtaining various results: positve correlaton between these two variables, others report a negatve correlaton, while some conclude that they are not statstcally signifcant.

Brine, Brown and Hacket (2007), in the Australian context, took a sample of 277 companies for the year 2005, using as a measure of social responsibility sustainability statements, and gave a value of 1 to those organizatons that practced, and 0 otherwise, while accountng performance measurement took into account the return on assets, return on equity and return on sales, thus concluding their work that did not fnd a statstcally signifcant relatonship between responsibility Corporate social and fnancial performance.

Tsoutsoura (2004) analyzed 422 companies covering a period from 1996 to 2000, considering The Domini 400 Social Index (DSI 400) as the indicator to measure social responsibility, taking the value of 1 if the economic entty was included in the DSI 400, and 0 if it was not, whereas employment, fnancial performance, return on assets, return on equity and return on sales, reported results in a statstcally signifcant positve relatonship between corporate social responsibility and fnancial performance of the company.

Moreover Saavedra (2011) makes a collecton of different research on this topic as well as the results obtained. She analyzes results that show a positve relatonship between corporate social responsibility and economic performance of enterprises other that no relatonship between these two variables, or even a negatve relatonship. Accordingly, Saavedra mentoned that the relatonship between CSR and fnancial performance is not yet defned but are more numerous studies have proven that there is a positve relatonship between CSR and proftability.

Frame of reference

Key features of the Mexican Stock Exchange

The Mexican Stock Exchange, S.A.B. de CV is a fnancial insttuton that operates by grant from the Ministry of Finance, in accordance with the Securites Market Act, in additon to observing the principles established in the Code of Best Corporate Practces issued by the Business Council and the Code of Ethics professional Community at Mexican Stock Exchange.

Currently (2012), 124 actve companies are listed. The CPI (Index of Prices and Quotatons) is the main indicator of the Mexican Stock Exchange, the performance expressed in terms of changes in the stock market price of a balanced sample, weighted and representatve of all shares traded on the Stock Securites and serves as the underlying fnancial products.

The serial number of shares comprising the sample Price Index (IPC) is 35 series, which may vary during the period covered by corporate actvity.

The sample used in the calculaton is made of the stocks in the different sectors of the economy and is presented in Table 1:

| Stock company | ||||

|---|---|---|---|---|

| Alfa | Elektra Gpo | GMexico | Kimberly Clark Mex | Soriana Organizacio |

| Ara Consorcio | Fomento Econ Mex | GModelo | Liverpool Puerto de | Televisa Gpo |

| Bimbo | Geo Corporacion | Gruma | Mexichem | TV Azteca |

| Cemex | GFBanorte | Ica Soc Controlad | Penoles Industrias | Wal Mart de Mexico |

And Table 2 shows the companies belonging to the BMV with distnctve CSR (and who meet the criteria of the models in this study):

| Company/Year | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | Sum |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Alfa | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 |

| ARA | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 1 | 1 | 5 |

| Bimbo | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 11 |

| CEMEX | 0 | 0 | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 8 |

| CocaCola FEMSA | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 6 |

| GEO | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 6 |

| GMODELO | 0 | 0 | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 8 |

| ICA | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 2 |

| MEXICHEM | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 3 |

| Peñoles | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 10 |

| Walmart | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 11 |

Methodology

We are applying the criteria of Collins, Maydew and Weiss (1997) methodology by considering the independent variables using historical data published in fnancial reports and consider the lagged independent variable at a tme (in a quarter afer the date of each independent variable).

Because the study is under cross-sectonal criteria and over tme, differences were taken into variables to be statonary series and do not have spurious regressions.

Research Hypothesis

First hypothesis: fnding signifcance in both fnancial accountng variables selected to assess impact on the stock price (one quarter afer the publicaton of informaton).

Second hypothesis: fnding signifcance of CRS in the stock price (one quarter afer the publicaton of informaton).

Models used in each scenario

The model to be considered for the frst hypothesis is:

Δ Pit+1 = α0it + α1itΔOEit + α2itΔFAit + εit

where:

Δ Pit+1: Change in price per share of frm i three months afer each quarter of the period t,

Δ OEit: Change in operatng expenses (previous year) of frm i in the period quarter t

Δ FAit: Change in fxed assets (previous year) of frm i in the period quarterly t, and

εit: Other relevant informaton of frm i in the quarterly period t, being orthogonal to Change in Change in operatng expenses and fxed assets.

Then we add the effect of considering the distnctve of Corporate Social Responsibility, in order to identfy if it has or not impact on the market. For the model considered for the second hypothesis is:

Δ Pit+1 = α0it + α1itΔOEit + α2itΔFAit + α3itΔCSRit + εit

where:

ΔPit+1: Change in price per share of frm i three months afer each quarter of the period t,

ΔOEit: Change in operatng expenses (previous year) of frm i in the period quarter t,

ΔFAit: Change in fxed assets (previous year) of frm i in the period quarterly t,

ΔCSRit: Presence or no (1 or 1) of the distnctve of Corporate Social Responsibility of frm i in the period quarterly t, and

εit: Other relevant informaton of frm i in the quarterly period t, being orthogonal to Change in Change in operatng expenses and fxed assets.

Characteristcs of the Database

The study period data concerning fnancial and accountng informaton and share prices, is separated into two sectons:

First block: (frst hypothesis)

From the frst quarter of 2000 to the third quarter of 2011 (being 47 quarterly periods). The purchasing power of the accountng and fnancial informaton (from the database Economatca in May 2012) is with the currency denominaton of constant Mexican pesos at April, 30th, 2012. The fnancial accountng variables are used at the end of each quarterly period and the share price used in the next quarter of the accountng data.

Second block: (frst hypothesis)

From 2000 to 2011 (11 annual periods).The purchasing power of the accountng and fnancial informaton (from the database Economatca in May 2012) is with the currency denominaton of constant Mexican pesos at April 30th, 2012. The fnancial accountng variables are used at the end of each quarterly period, the distncton of being recognized as a socially responsible company is treated as dummy (1 = if it has the distnctve and 0 = if you do not) and the stock price is used in the next quarter of the accountng data.

Defniton of Variables

The independent variables are two fnancial statements taken from the consolidated fnancial statements and a category (dummy):

- "Change in operatng expenses" in the Income Statement as a measure of efciency by controlling the internal processes of the company, meaning be efcient if reduced from the previous year.

- "Change in the amount of Fixed Assets" Balance Sheet, as a measure of investment in the long run (only in the company belonging to the fnancial sector are detailed the capton "Machinery and equipment" for this purpose, since the other items were different, by increasing the amount from the previous year are dedicatng resources to grow in the long term investment (both tangible and intangible items).

- dummy variable refers to whether or not it has the badge awarded by CEMEFI: CSR (annual distnctve), as a strategic reference of innovaton revised in secton 2.

The dependent variable is the price per share. By this concept, we used the closing price of the Mexican Stock Exchange, one quarter afer the close of each of the study periods of independent variables.

The companies that meet the characteristcs of the variables required, under each hypothesis tested are 20 stocks for the frst hypothesis, it is presented in Table 3:

| Company Name | Economic Sector | Company Name | Economic Sector |

|---|---|---|---|

| Alfa | Basic & Fab Metal | Gruma | Food & Beverage |

| Ara Consorce | Construction | Ica Soc Controlad | Construction |

| Bimbo | Food & Beverage | Kimberly Clark Mex | Pulp & Paper |

| Cemex | Nonmetallic Min | Liverpool Puerto de | Trade |

| Elektra Gpo | Trade | Mexichem | Chemical |

| Fomento Econ Mex | Food & Beverage | Penoles Industrias | Mining |

| Geo Corporacion | Construction | Soriana Organization | Trade |

| GFBanorte | Finance and Insurance | Televisa Gpo | Other |

| GMexico | Mining | TV Azteca | Other |

| GModelo | Food & Beverage | Wal Mart de Mexico | Trade |

And 11 companies for the second hypothesis, is presented in Table 4:

| Company Name | Economic Sector | Company Name | Economic Sector |

|---|---|---|---|

| Alfa | Basic & Fab Metal | GModelo | Food & Beverage |

| Ara Consorce | Construction | Ica Soc Controlad | Construction |

| Bimbo | Food & Beverage | Mexichem | Chemical |

| Cemex | Nonmetallic Min | Penoles Industrias | Mining |

| Fomento Econ Mex | Food & Beverage | Wal Mart de Mexico | Trade |

| Geo Corporacion | Construction |

Characteristcs of the econometric variables

For the frst model, the econometric analysis was performed by EGLS panel data, fxed staton considered effectve and defned SUR (considering each company as seemingly unrelated equaton).

For the second model, we performed the econometric analysis of panel data least squares (leaving the 3 independent variables), afer being weighted by each staton (leaving the 3 independent variables) and fnally evaluatng only the independent variable of CSR.

Empirical Results

First hypothesis

Table 5 presents the results of the frst model, which were found to be signifcant independent variables:

- Change in operatng expenses, with the coefcient sign, as expected. Because if they decrease operatng expenses, they were expected to have positve effect on the share price and that's what happened, so the coefcient is negatve.

- Change in fxed assets, with a sign on the coefcient, as expected. Given that an increase in investment is expected to have positve effect on the share price.

| Variable | Coefficient | p-value |

|---|---|---|

| C | 45.07855 | 0* |

| GO | -0.039444 | 0* |

| AF | 0.0000644 | 0* |

Of the two factors, the only signifcant operatng expenses, taking evidence of operatonal process efciency (over the previous year).

Second hypothesis

In Tables 6 and 7 presents the results of the second model, under a panel data analysis where we found that the only signifcant independent variable was the presence of the Badge of CSR signed in the coefcient, as expected. How long has this flag been expected to have positve effect on the share price. Table 6 is considering a panel data model under OLS and Table 7 is considering a weighted cross under EGEL:

| Variable | Coefficient | p-value |

|---|---|---|

| GO | 0.147728 | 0.5642 |

| AF | 0.000469 | 0.8203 |

| CSR | 60.32731 | 0* |

| Variable | Coefficient | p-value |

|---|---|---|

| GO | 0.077452 | 0.2364 |

| AF | 3.99E-05 | 0.9352 |

| CSR | 42.37642 | 0* |

Conclusions

In this paper we analyzed the exploratory signifcance of independent variables (related to the two approaches to measuring innovaton with fnancial performance), in light of the criteria of the Manual of Oslo and Bogota, in an analysis of 47 periods quarterly, from 2000 to 2011.

Also, we added to the inital model (1), as the independent variable distnctve presence of CSR (model 2), that is a strategic reference of innovaton revised in secton 2, and was found to be signifcant in the impact of share price three months later. This variable is important because of the growing interest in the company to have business with this flag, which also rewards the stock market in terms of the 11 stocks studied from 2001 to 2011.

These results provided empirical evidence of the interrelaton of CSR on the stock market returns of the selected companies analyzed on this study. And we also found relevance in fnancial statements of general changes of innovaton practces, though we measured the econometrical signifcance (under panel data analysis) in short term (three months afer), these results represent a proxy of the reacton of the market to this kind of fnancial decisions of strategic paterns of medium or long impact.

We considered this study as the beginning of a line of studies on the impact of fnancial variables (investment related innovaton made public enterprises), including the distnctve CSR (as part of strategy to customers, as with the stock market), in additon to leading to have this awareness in the performance of the stocks. The contributon of this exploratory analysis is that it provided a quanttatve reference of the relaton of the considered variables, for selected companies of Mexico, of the effect measure of innovaton and CSR impact on the stock market.

End Notes:

- The Oslo Manual is a guide to the applicaton and interpretaton of data on innovaton, supported by the OECD (Organizaton of Economic Co-operaton Development).

- Manual de Bogotá focuses on implementng the Oslo Manual in the Latn American reality, supported by the OAS (Organizaton of American States).

References

- Abreu, J. (2009). Preliminary report of research on Corporate Social responsibility, explained by the Neuroeconomics: Daena model. Revista Daena. Internatonal Journal of Good Conscience, 4 (1), 87-115.

- Accenture (2010). A reliable proposal, how to win credibility with the consumer through sustainability and compettve advantage. Business Management Magazine, September, 36-40.

- Brine, M.; Brown, R. and Hacket, G. (2007). Corporate Social Responsibility and Financial Performance in the Australian Context. Economic Round-up, Autumn, 47-58.

- Cajiga C. (2010). The concept of Corporate Social responsibility. (Spanish). Center Mexican philanthropy. Recovered from htp://www.cemef.org/esr/pdf in February 2012.

- Cadinaels, E. and Van Veen-Dirks, P. (2010). Financial versus non-fnancial informaton: the impact of informaton organizaton and presentaton in a balanced scorecard. Accountng, Organizatons and Society, 35 (6), 565-578.

- Carroll, A. (1991). The pyramid of corporate social responsibility: toward the moral management of organizatonal stakeholders. Business Horizons.

- Collins, D. W., Maydew, E. L., Weiss, I. S. (1997). Changes in the value-relevance of earnings and book values over the past forty years. Journal of Accountng and Economics, 24, 39-67.

- CONACYT-INEGI (2001). Survey on innovaton. Web reference in INEGI.

- Chavarria, M. (2009). Corporate social responsibility (CSR) and communicaton: the agenda of the large Mexican companies. Sign and thought, 28 (55), 201-217.

- Iselin, E. Mía, L. Sands, J. (2008). The effects of the balanced scorecard on performance: the impact of the alignment of the strategic goals and performance reportng. Journal of General Management, 33, 71-85.

- Kaplan, R.S., Norton D. (1996). Translatng strategy into acton: The Balanced Scorecard, Cambridge, MA: Harvard Business School Press.

- Neely, A. (2002). Business Performance Measurement - Theory and Practce, Cambridge University Press, Cambridge. 304-318.

- OECD (1997). Proposed Guidelines for Collectng and Interpretng Technological Innovaton Data, "Oslo Manual", Eurostat.

- RICYT / OAS / CYTED COLCIENCIAS / OCYT (2001). Standardizaton of indicators of technological innovaton in Latn America and the Caribbean, "Manual of Bogota".

- Salgado Mercado, P., & García Hernández, P. (2007). Social responsibility in companies in the Valley of Toluca (Mexico). An exploratory study. Estudios Gerenciales, 23 (102), 119-135.

- Saavedra, M. L. (2011). La Responsabilidad Social Empresarial y las fnanzas, Cuadernos de Administración, 27 (46), 39-54.

- Schumpeter, E.B. (1938). English Prices and Public Finance, Review of Economic Statstcs, 20, 21-37.

- Tsoutsoura, M. (2004). Corporate social responsibility and fnancial performance, Working paper series of Berkley University, 1-21. Permanent link: htp://escholarship. org /uc/item/111799p2

- Yu, L. Perera, S and Crowe, S. (2008). Effectveness of the balanced scorecard: the impact of strategy and causal links, Journal of Applied Management Accountng Research, 6, 37-55.